Published on May 22, 2024 by Sreeja Roy Chowdhury , Debarati Dutta , Mahesh Agrawal , Jenil Mehta , Archana Anumula and Somya Dixit

Price performance over April 2024

Global market overview

The equity market retreated in April even as the earnings season started on a strong note with most of the companies reporting better-than-expected earnings. Expectation of a rate cut soon and geopolitical concerns weighed on sentiment. Asia ex-Japan performed better. Commodities continued the positive run led by industrial metals on supply concerns and stronger demand. Gold could remain volatile, taking cues from geopolitics and expectations of Federal Reserve (Fed) rate cuts. Tensions in the Middle East could continue to provide a floor for energy prices.

The USD continued to trade strongly against major currencies as expectations of a rate cut eased. Inflation remained higher than the Fed's target rate, triggering the agency to adopt a hawkish tone at its last meeting. Speculation that the European Central Bank (ECB) and the Bank of England (BoE) could start rate cuts before the Fed could continue to support the USD in the short term. However, we believe that most regions' rate cuts remain data-dependent and that uncertainty could persist in the coming months.

Charts for the month

Source: Investing.com, IMF April 2024 outlook

Equity market

-

Review:

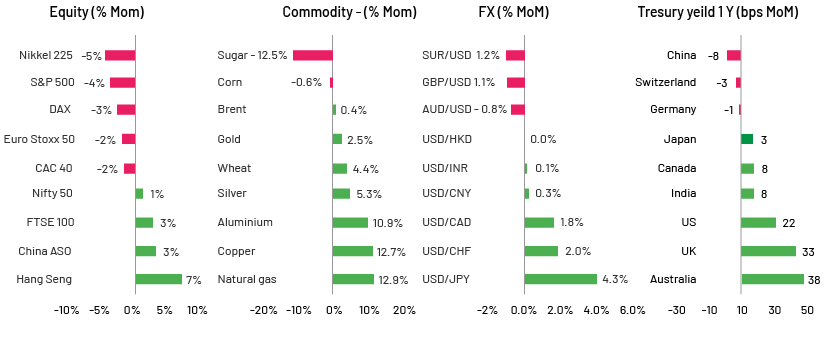

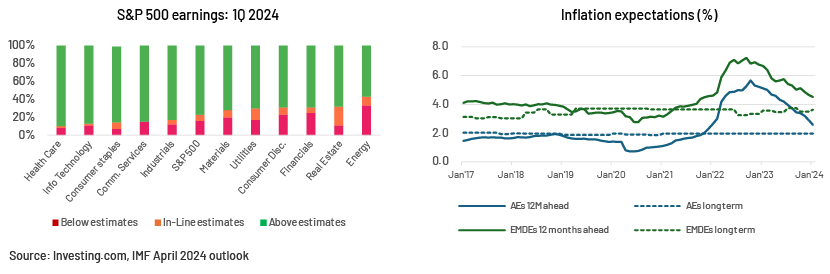

April saw a widespread correction in global equities, notably a 7% drop in the US small-cap index and a 4% decline in the S&P 500, driven by readjusted rate-cut expectations and concerns over higher interest rates for longer. Despite this, the US market experienced a robust earnings season, according to FactSet,i with 77% of companies reporting actual EPS above estimates, matching the five-year average. The healthcare and information technology sectors performed particularly well. European indices also corrected, except for the UK Index (FTSE100), which rose 2.7% due to strength in energy and value stocks and increased earnings expectations.

-

Outlook:

In May, investor focus would be on China and Hong Kong, where efforts to revive property markets could reveal cheap value opportunities. Geopolitical tensions and speculation around further rate cuts would also dominate discussions. In addition, attention will likely be on expectations of a BoE rate cut, potentially fuelling a rally in UK stocks. Monitoring market trends remains crucial amid the ongoing volatility.

Commodities market

-

Review:

Industrial metals performed relatively well, with the London Metal Exchange (LME) Index rising 13% m/m in April, as metal prices benefited from tightening supplies, shrinking inventories and recovering demand. Copper led the gains among base metals, with prices moving above USD10,000/t towards the end of the month. Prices rose 12.7% m/m in April, primarily due to disruptions in mine supply and expectations of robust demand this year, especially from the green energy sector. Among other base metals, prices of aluminium also gained sharply last month as the LME banned the delivery of new Russian metals to the exchange. Meanwhile, in energy, US natural gas performed well, with prices rising by 13% m/m last month as expectations of warmer-than-usual temperatures boosted the nation's demand outlook. Meanwhile, in agri commodities, sugar prices fell sharply, by 12% m/m in April, on improved supply, supported by weather in the main producers - Brazil, Thailand and India.

-

Outlook:

Industrial metals are expected to continue to perform well, as fundamentals remain supportive. However, risks from China continue as copper inventories remain elevated, while the Fed's higher-for-longer narrative could put downward pressure on copper prices. The gold market is expected to remain volatile on mixed expectations in the market about the Fed starting to cut rates in June. Meanwhile, crude oil prices are expected to perform better over the coming weeks due to continued escalations in tensions in the Middle East.

FX market

-

Review:

The USD rallied over most of April due to a firm inflation print in March, triggering expectations that the Fed may adopt a hawkish tone in May. However, the markets have interpreted Fed Chair Powell's speech on 1 May as a dovish stance, as it ruled out rate-hike scenarios and reinstated the possibility of easing rates in 2H 2024. As a result, the USD came under bearish pressure. The JPY remained weak in April, with the USDJPY crossing 160, but by the last week of the month, it had rallied below 160. Although not officially announced by the Japanese authorities, markets interpreted this a result of intervention. This, coupled with the USD sell-off after the FOMC meeting, favoured the JPY, exerting pressure on the USDJPY. The EUR remained broadly stable as regional growth continues to recover. On the other hand, Asian currencies were under pressure from the USD as markets slashed expectations on the number of Fed rate cuts this year.

-

Outlook:

The JPY will likely remain subject to intervention by the financial authorities as its struggle in the free market against the USD continues. Markets expect a hawkish stance by the Reserve Bank of Australia (RBA) in May given stickier inflation of late, likely underpinning gains in the AUD after the policy meeting. US payrolls data released on 03 May has renewed expectations of rate cuts this year. The markets believe that softer labour-market data and Powell's indication that the Fed remains data-dependent could add bearish pressure on the USD in the coming months. Policy divergence from the Fed's could exert bearish pressure on the EUR and the GBP, as the respective central banks are slated to start easing policy rates earlier than the Fed. A longer hold by the Fed would also mean that Asian currencies may continue to depreciate against the USD.

Debt market

-

Review:

April witnessed a large sell-off in bond markets across major economies. US 10y Treasury yields skyrocketed at end-April (+49.2bps from end-March) owing to sticky inflation and markets expecting the Fed to keep rates higher for longer. This sharp rise in US yields had a positive spillover effect on the European bond market. German 10y bund yields, the Eurozone's benchmark, moved upwards, breaching the 2.5% mark in April. UK gilts rose more than 40bps from end-March, the highest jump since the beginning of the year. In Japan, bond yields remained higher as of end-April even as the Bank of Japan (BoJ) kept rates unchanged; markets now expect the BoJ to hike rates in 3Q 2024.

-

Outlook:

Yields are expected to keep moving upwards in May as the US economy remains resilient with the Fed keeping rates unchanged at the May meeting. The markets are now pricing in one rate cut in 2024. The IMF's April outlook shows that although inflation is falling in advanced economies, it could still stay higher than the long-term target of 2% over the next 12 monthsi. German bund yields and UK gilts are also expected to remain elevated, as markets now expect fewer rate cuts by the ECB and the BoE this year. JGB yields are expected to remain under upward pressure, driven by the BoJ's rate-hike path and pace of quantitative tightening.

Key data releases:

| Indicator | Country |

Release date |

Consensus (actual) |

Previous |

| CPI (% y/y, April, final) | US |

15-May-24 |

- |

3.5% |

| Eurozone |

17-May-24 |

2.4% |

2.4% |

|

| UK |

22-May-24 |

- |

3.2% |

|

| China |

11-May-24 |

0.1% |

0.1% |

|

| Japan |

24-May-24 |

- |

2.7% |

|

| Manufacturing PMI (Index, May, flash) | US |

23-May-24 |

- |

50.0 |

| Eurozone |

23-May-24 |

- |

45.7 |

|

| UK |

23-May-24 |

- |

49.1 |

|

| China |

31-May-24 |

- |

50.4 |

|

| Japan |

23-May-24 |

- |

49.6 |

|

| Retail sales (% m/m, April) | US |

15-May-24 |

0.4% |

0.7% |

| Eurozone* |

7-May-24 |

0.6% |

0.8% |

|

| UK |

23-May-24 |

- |

0.0% |

|

| China^ |

17-May-24 |

3.8% |

3.1% |

|

| Japan |

31-May-24 |

- |

13.5% |

|

| GDP (% q/q, Q1, 2nd estimate/final) | US |

30-May-24 |

- |

0.4% |

| Eurozone |

15-May-24 |

0.3% |

-0.1% |

|

| UK |

10-May-24 |

0.4% |

-0.3% |

|

| Japan |

16-May-24 |

- |

0.1% |

|

| Policy rate decisions (%, May) | US |

1-May-24 |

5.50% (A) |

5.50% |

| UK |

9-May-24 |

5.25% |

5.25% |

|

| China** |

20-May-24 |

- |

3.45% |

|

| Major events due in May | ||||

| ECB minutes for April | Eurozone |

10-May-24 |

||

| BoJ MPC minutes for April | Japan |

2-May-24 |

||

| FOMC minutes for April | US |

22-May-24 |

||

| General elections (Phases 3, 4, 5 and 6) | India |

07, 13, 20, and 25 May |

||

| Note: * Mar release; ^ % y/y; ** 1y LPR. Dates are reported in local time zone | ||||

| Source: National Statistical Offices, Trading economics | ||||

How Acuity Knowledge Partners can help

Our large pool of macro experts are experienced in providing research and strategic support across the value chain. We have partnered with macro research firms, global investment banks, asset management firms and hedge funds over the years, working closely with their research, strategy and investment teams to provide them with the information and analysis required in the investment decision-making process.

We also provide tech-enabled data management solutions and modelling and analytics services covering macroeconomics, FX and commodities forecasts [Macro Economic Research, FX, and Commodities Analysis | Acuity Knowledge Partners (acuitykp.com)].

Source

What's your view?

Thank you for sharing your Comments

Share this on

About the Authors

Sreeja has over 5 years of experience in economics and equity research. She has been with Acuity Knowledge Partners (Acuity) since 2018, providing sell-side research support to a global investment bank. At Acuity, she is part of the Cross-Asset Research Support team, specializing in macroeconomics research, high-frequency data tracking and financial modelling. Prior to joining Acuity, she worked as an equity research analyst with Zacks Research. Sreeja holds a Master of Science (Economics) from the University of Calcutta, India.

A postgraduate in Economics with over 7 years of experience in economic research. Currently at Acuity Knowledge Partners, is Delivery Manager, supporting a leading investment bank specializing in macroeconomics research. Responsibilities broadly involve analyzing country-specific macroeconomic data, tracking macro indicator releases and their evolution. Debarati holds a Master of Arts (Economics) from Madras Christian College (Autonomous), India and Bachelor of Science (Economics) from the University of Calcutta, India.

Mahesh has over 14 years of experience in commodity and macroeconomic research and has been associated with Acuity Knowledge Partners (Acuity) since September 2012. At Acuity, he supports a leading European investment bank’s commodity research desk in analysing commodity markets, preparing research notes and creating presentations for conferences and client interactions. Mahesh holds a master’s degree in Science (Energy Trading) from the University of Petroleum and Energy Studies, Gurugram, and a Bachelor of Science from Bikaner University, Bikaner.

Jenil Mehta is part of the Specialized Solution team at Acuity Knowledge Partner. He is part of a team of Asian equity derivatives strategists at one of the leading Japanese investment banks. He contributes to highlighting and publishing trade ideas, bespoke reports, and idea back testing based on fundamental and quantitative analysis. Before working here, he was a fixed-income derivatives trader and research analyst for North American and Brazilian markets. Jenil holds a bachelor’s degree in computer engineering and has passed all three CFA Levels.

Archana has over 16 years of experience in economics research, with proficiency in areas such as writing country-specific economic reports, real-time macroeconomic indicator release coverage and building and maintenance of large datasets. She has been with Acuity Knowledge Partners since 2011 and currently manages the Macroeconomics Research teams for two top-tier global firms. She is responsible for hiring, client engagement and account management. She is also in charge of business development for the Macroeconomics Research sub-vertical under Quantitative Services. Archana holds a Master of Arts (Economics) from St Joseph‘s College (Autonomous), India and a Bachelor of Commerce from Bangalore University, India.

A management postgraduate with over 12 years of experience in the Commodities Market. Well conversant with the fundamental aspects, inter-market relationships and Geo-political issues impacting the market. Currently at Acuity Knowledge Partners as Delivery Manager responsible for providing market analysis and assisting the client in preparing research analysis for the commodities (Energy, Metals & Agri). Well-acquainted with the use of data sources such as Thomson Reuters and Bloomberg. Somya holds a postgraduate degree in finance and a bachelor's degree in electronics engineering.

Blog

Blog

Interest Rate Divergence in 2024: A Global Conte....

Interest rates are diverging sharply in major economies, most notably in the US and the Eu....Read More

Blog

Blog

Impact of Israel-Iran war on oil supply and pric....

What happened and when… On 13 April 2024, Iran began its first full-scale military air ....Read More

Blog

Blog

Global Market Insights – December 2024: US

Global market overview Donald Trump’s victory in the US presidential election provi....Read More

Blog

Blog

Global markets insights – November 2024: Tr

Global market overview The global equity market retreated last month as geopolitical ....Read More

Blog

Blog

Global markets insights – October 2024: Fed

Global market overview China’s equity market gained favour among investors last month....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox