Published on August 3, 2020 by

Black-swan events, including the US sanctions on Iran and Venezuela, geopolitical tension in the Middle East and the COVID-19 pandemic, have been driving oil and gas prices in recent years. The pandemic has negatively affected global economic activity, eliminating global oil demand growth potential. Global liquid fuel production declined significantly to 95 million barrels per day (mbbl/d) in 1Q 2020, representing a 6.4mbbl/d dip on a y/y basis, and fell further to 84mbbl/d in 2Q 2020, a drop of 17.3mbbl/d on a y/y basis. Containment measures, including global lockdowns, particularly in the US, Europe, India and the Middle East, have resulted in a negative demand shock for gasoline, jet fuel and other fuels.

On the supply side, global oil production fell sharply in June and stood 13.7mbbl/d below the April level. The compliance rate with the OPEC+ supply agreement was 108%. This was supplemented by substantial market-driven cuts, mainly in the US. US crude oil production in June averaged 11.0mbbl/d, down 1.9mbbl/d from the record high in November 2019.

As road and air travel fell sharply with the global lockdowns in the first quarter and early in the second quarter of this year, global liquid fuel consumption dipped faster than production. Owing to the production-consumption imbalance of liquid fuels, the US Energy Information Administration (EIA) estimates that global oil inventories increased by almost 1.3bn bbl from the start of 2020 through the end of May.

COVID-19 impact on oil and gas companies

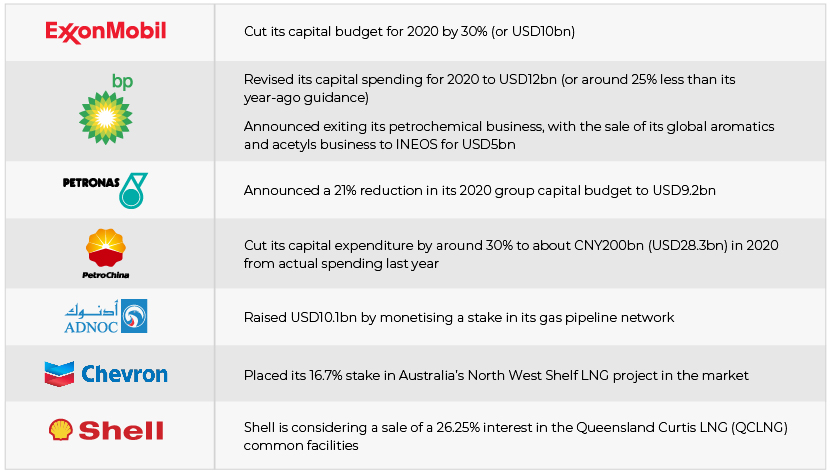

The oil price crash has led to severe stress on exploration and production (E&P) companies. E&P companies have taken, or plan to take, financial measures to control the damage caused by the pandemic, including reducing budgets and delaying projects and divestments. The International Energy Agency (IEA) expects upstream investment from oil companies to plunge 32% y/y in 2020 to USD335bn from USD490bn in 2019. We list below some of the measures E&P companies have taken:

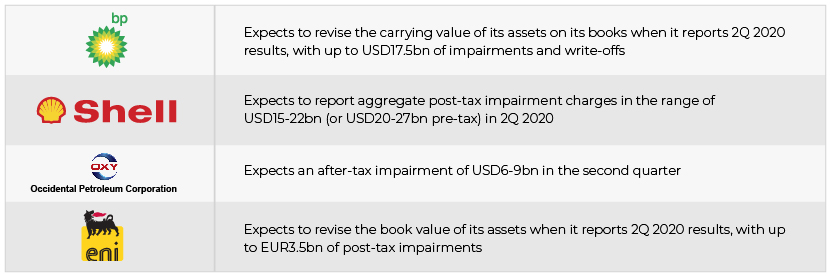

Some companies expect to book significant impairments in 2Q 2020:

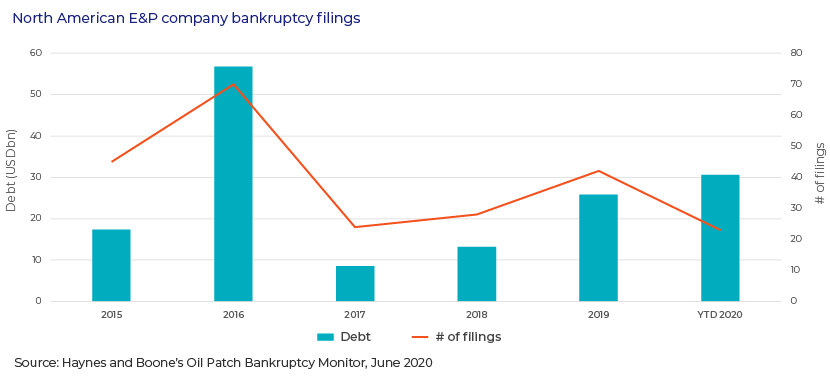

As E&P company revenue has crashed, along with crude and natural gas prices, many industry observers expect a flood of bankruptcies in the upstream sector of the business. In its Oil Patch Bankruptcy Monitor, Haynes and Boone listed 23 bankruptcy filings of US E&P firms in the first six months of 2020, totalling USD31bn of debt. The list features well-known names such as Chesapeake Energy and Whiting Petroleum. Haynes and Boone expect a substantial number of E&P companies to seek protection from creditors amid bankruptcy even if oil prices recover over the next few months.

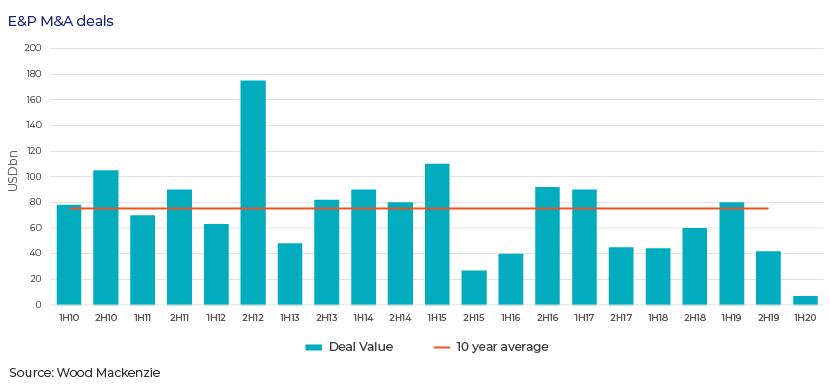

M&As plummet to record low

E&P M&A deals have plummeted following a period of prolonged low oil prices and a steep fall in demand due to the COVID-19 crisis. With no deals above USD1bn, the first half of 2020 saw the lowest deal volume in the past several decades. Monthly average spending on deals has been just 5% of the run rate of the past 15 years.

In the wake of the pandemic, a number of factors favour an increase in acquisitions. Valuations are at their lowest since 2009. Chevron announced on 20 July 2020 that it will acquire Noble Energy for USD13bn. This is the first large-scale corporate oil and gas acquisition since the start of the pandemic. It could also be the start of a new wave of corporate consolidation.

COVID-19 impact on M&A deal structuring

Contingent payments are being increasingly used in new deals, and previously announced deals are being revised

-

June 2020: Energean restructured the deal to acquire Edison assets by dropping the Algerian and Norwegian assets from the deal and adding a contingent payment of up to USD100m based on prices

-

May 2020: Santos revised its deal to acquire ConocoPhillips Australia assets and increased the contingent payment to USD200m from USD75m by reducing upfront consideration

-

April 2020: Hilcorp renegotiated terms of the deal with BP to change the structure and earnout arrangements

-

April 2020: Total’s acquisition of Tullow Uganda assets includes a contingent payment of USD75m at the final investment decision (FID) and additional unspecified contingent payments triggered when Brent prices are above USD62/bbl

Several deals collapsed to preserve financial flexibility in the current environment

-

July 2020: Premier Oil dropped acquisition of a further stake in the Tolmount project from Dana Petroleum

-

May 2020: Total discontinued acquisition of Occidental Petroleum’s assets in Ghana

-

May 2020: Neptune Energy terminated the agreement to acquire Edison E&P’s UK and Norwegian subsidiaries from Energean

Early signs of recovery

China, the world’s second-largest economy, returned to growth in 2Q 2020 – one of the earliest signs of recovery from the fallout of the coronavirus pandemic. The economy grew 3.2% y/y in the three months ending June 2020. US payrolls grew by 4.8m in June; this was the second month of gains after a loss of over 20.0m in April. India’s Manufacturing Purchasing Managers’ Index, compiled by IHS Markit, stood at 47.2 in June compared with 30.8 in May on a seasonally adjusted basis.

Global surveillance data for the week of 21 June 2020 confirmed that an average of 34,300 unique aircraft were operating daily. This is approximately 10,000 fewer than at the same time in 2019 but 14,000 more than were operating in mid-April 2020, when traffic was at its lowest.

As the economies began emerging from their lockdowns, petroleum and other liquid-fuel consumption witnessed an upward movement (global consumption in June was up 10mbbl/d from April levels, according to EIA estimates). Supply and demand estimates shifted global oil markets from 21mbbl/d of oversupply in April to inventory draws in June. The EIA expects these inventory draws to push oil prices upwards, which would be partly offset by existing high oil inventories, particularly in 2H 2020.

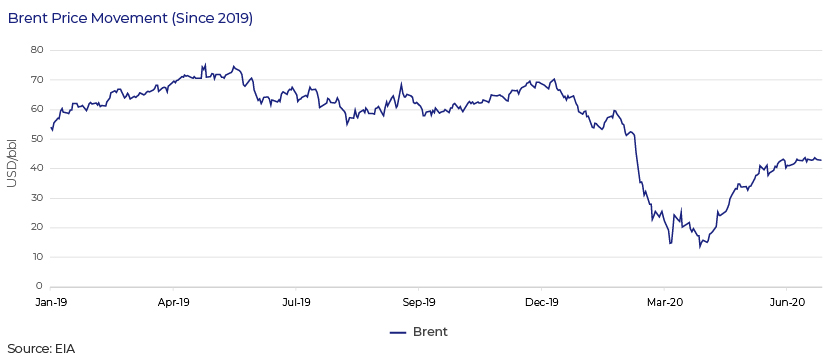

Increased travel and a rebound in economic activity led to a strong recovery in crude oil prices in May and June. Brent oil prices more than doubled to USD43/bbl on 20 July 2020 from the low of USD17/bbl on 21 April 2020 as fuel demand picked up and crude supply was reined in.

On 15 July 2020, OPEC+ agreed to lift certain output restrictions, stating that global demand for oil is beginning to recover. Starting in August, the member countries will ease their collective output cuts to 7.7mbbl/d from the current 9.7mbbl/d (which took effect in May 2020).

We believe the COVID-19 crisis will have a deep impact on global oil and gas businesses. While the depth and duration of this crisis are uncertain, the industry could now enter an era defined by intense competition, technology-led rapid supply responses, tepid demand, a high level of ESG scrutiny and energy transition. However, in most scenarios, the oil and gas sector will likely remain a multi-trillion-dollar market for decades to come. With a 57% share in primary energy demand (in 2019), oil and gas is too important to fail.

How Acuity Knowledge Partners can help

We have a large pool of energy experts with a wide range of experience covering the investment banking, corporate consulting, private equity and commercial banking practices. To help our clients navigate both the people and business impact of COVID-19, we have created a dedicated hub containing a variety of topics including our latest thinking, thought-leadership content and action-oriented guides and best practices. Our experience aligns with that of turnaround consulting firms, offering strategies to improve operations, restructure and navigate crises.

We also have the capability to perform deep research across the energy value chain, including upstream, midstream, infrastructure, oilfield services, refining and petrochemicals, marketing, macroeconomic outlook, commodity outlook and ESG factors.

References

Company information

OPEC Monthly Oil Market Report – June 2020

https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

https://www.eia.gov/dnav/pet/hist/rbrteD.htm

What's your view?

Thank you for sharing your Comments

Share this on

Comments

19-Aug-2020 02:30:08 am

Hi Mrutyunjay, indeed a nice read. Have a few personal opinion - Since M

Blog

Blog

Top trends driving momentum in equity capital ma....

Last year was a transformative year, fuelled by rapid technological advancement amid ingen....Read More

Blog

Blog

China’s imports of Japanese food products decl....

Background China has consistently been one of Japan's most important trading partners: Ja....Read More

Blog

Blog

The mystery of black swans and how to prepare fo....

In the realm of global financial markets, there exist fascinating phenomena known as “bl....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox