Published on April 2, 2025 by Jatin Aggarwal

In November 2024, all eyes were on the US presidential elections because the chances of Trump coming back to power were high, and countries such as Mexico, Canada and China were concerned about a potential tariff war.

The fear played out as Trump's "America First" foreign policy accounted for most of the Republican Party’s electoral success. The trade goals – such as correcting the trade imbalance, addressing unfair trade practices and boosting the US economy and its manufacturing sector – were fairly consistent with those during his first term. On the first day of his second term, President Trump made tariffs a top priority, proposing a 10% tariff on all imports to the US, with tariffs of 25% on allies such as Mexico and Canada. When asked whether he would impose a universal tariff, he responded, "I may, but we are not ready yet."

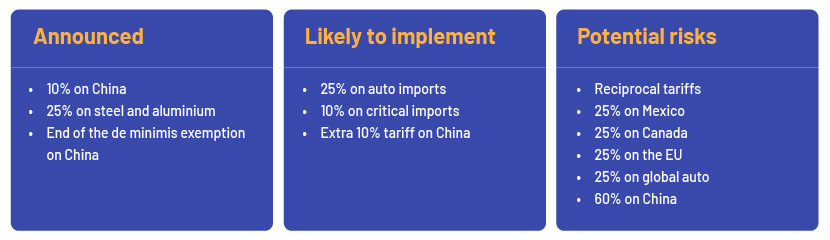

Since then, there has been a lot exchanged between these countries, with Mexico and Canada even warning of retaliation. Just two days after imposing a 25% tariff across the board on Canada and Mexico, the US paused tariffs on goods and services compliant with the United States-Mexico-Canada Agreement (USMCA) until 2 April 2025. In response, Canada imposed duties on c.USD20bn worth of US goods. The EU was not spared; President Trump imposed a 25% tariff on steel and aluminium imports, affecting >EUR18bn worth of EU exports. The EU retaliated by imposing tariffs on >EUR26bn worth of US exports including a 50% duty on US bourbon whiskey. He has warned of imposing a 200% tariff on champagne, wine and other alcoholic products if the EU does not pull back. In the latest development, President Trump has announced 25% tariff on all the auto imports in the US, effectively 3 April 2025. The White House expects this measure to generate c.USD100bn annually for the US.

Summary of tariffs in President Trump’s second term:

President Trump's stance on China has been very clear since the start of his first presidential term, i.e. that the US will enter a trade war with China to demonstrate its global dominance and protect domestic interests. A 10% tariff was already imposed on Chinese imports; this was increased by 10% (on 4 February 2025), with a 25% tariff on steel and aluminium (on 12 March 2025). The Trump administration plans for 60% or more tariffs on China. Although China has warned of retaliation, its ability to do so is limited, as its exports to the US were worth c.USD440bn last year versus c.USD144bn worth of imports. To counter the US tariffs, China imposed a 15% tariff on US farm exports and is looking for non-tariff options including going after companies such as Google and Nvidia that rely on Chinese markets and manufacturers through antitrust probes, banning gene sequencer imports from Illumina, etc. China could also manipulate the exchange rate by weakening the yuan against the USD, which would hurt US importers. Furthermore, if China decides to reduce exports of rare earth metals, which are used in everything from semiconductors to electric vehicles (China accounted for c.70% of the metallic elements used globally in 2024), this would disrupt the global supply chain.

Most of the tariff actions announced by President Trump are targeted at the US's largest trading partners, but he has been postponing the final implementation of such tariffs. In context, he also warned of such tariffs on Mexico in 2019, but these were never put into action. The proposed tariffs on Mexico and Canada are rather seen as negotiation tactics by President Trump, but tariffs on steel and aluminium are to likely be imposed given his constant comments about protecting domestic industries.

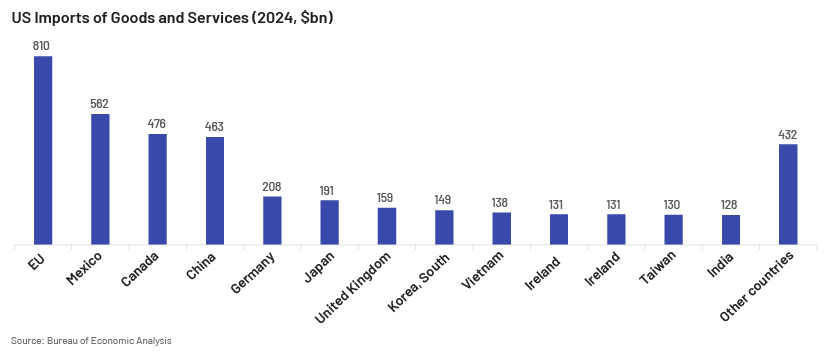

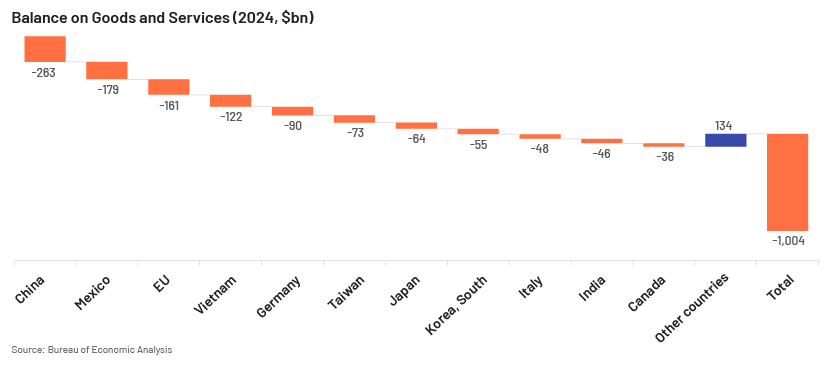

Being a businessman at heart, President Trump believes tariffs are bad and foreigners are taking advantage of the US through unfair trade practices. The US balance of goods and services was -USD1tn in 2024, with China, Mexico and the EU accounting for c.60% of this deficit. However, President Trump fails to understand the economics of a trade deficit and how the US notion of "Made in the USA" results in investments more than domestic savings, leading to a trade deficit that the US has been registering every year since 1975.

In terms of the current scenario, India seems to be somewhat exempt from the ongoing tariff war, with its focus mainly on the US’s major trading partners. If the US imposes reciprocal tariffs on India, it would lead to only a 3-3.5% decline in India’s exports to the US, according to SBI Research. India's alternative routes to export to the US and its diversified exports shield it from a major impact from the imposition of tariffs. The tariff war could rather be a blessing in disguise for India’s exports, as India has an opportunity to gain an edge in US markets as other exporters face higher tariffs. It also has the opportunity to strengthen its bilateral/regional alliances, pursuing favourable trade agreements and leveraging this global shift as global trade starts to become more region-centric.

This tariff war has shaken the global economy and disrupted the global demand/supply balance. Some industries are facing mounting losses while some are capitalising on these. Domestically, the decision is a boon to US steel and aluminium producers, with prices of steel and aluminium skyrocketing already. However, due to their heavy reliance on international supply chains, US automakers are taking a big hit. Tariffs could increase the production cost of a vehicle by c.USD400, according to Barclays. Companies such as Apple and Tesla that depend heavily on China for their production would also suffer. Higher tariffs on Chinese imports to the US are leading to a “China shock”, with China flooding global markets with cheap goods, leading to significant industry disruption and unemployment.

Conclusion

Markets are considered to be a weighing machine, and they have already started to react to these developments, but tariff risk prevails, continuing to cast a shadow over global markets. Global pandits have asked everyone to buckle up, as things remain even more unpredictable in President Trump's second term. All eyes are on 2 April 2025, when reciprocal and other planned tariffs are set to kick in. President Trump calls this “Liberation Day” but has hinted at some flexibility in imposing these duties, with room for discussion with trading partners. It is not yet clear whether he will opt for a uniform tariff or a reciprocal tariff, but global trade is set for a major shift. The escalating trade war has ignited fear of an economic slowdown in the US. Due to prevailing uncertainties, the Fed has raised inflation projections to 2.7% from 2.5% previously and lowered the GDP growth forecast for the year to 1.7% from 2.1% projected in December last year. An escalation of this tariff war is not inevitable, and global leaders could strike a good bargain and negotiate for good. If it escalates, the repercussions would be substantial, not just for the countries facing tariffs but also for the US.

How Acuity Knowledge Partners can help

We provide bespoke research and analytics services to financial institutions, consulting companies and asset managers for identifying global themes and capitalising on opportunities across the industry value chain. Our large pool of CAs, MBAs and CFAs help a diversified global client base, providing a wide range of services including financial modelling, deep-down fundamental research and market and industry research.

Sources:

-

Why Trump is imposing reciprocal tariffs on April 2 – The Times of India

-

Trump ends China's de minimis trade loophole for low-cost goods. What is it?: NPR

-

Trump's 25% EU tariffs rattles European shares, Wall Street mixed | World News – Business Standard

-

Trump says he will introduce 25% tariffs on autos, pharmaceuticals and chips | Reuters

Tags:

What's your view?

Thank you for sharing your Comments

Share this on

About the Author

Jatin is an equity research professional with over 9 years of industry experience. Over the years, he has led various client engagements with different buy-side and sell-side firms globally. He has expertise in conducting fundamental research, writing reports, and building financial models. Currently, he is working with a US based hedge fund and assisting them in Equity Capital markets (ECM). Jatin has cleared all three levels of CFA (USA) and done MBA in Financial Analysis. He has also earned the Financial Modelling & Valuation Analyst (FMVA®) certification provided by CFI institute of Canada.

Blog

Blog

Factors impacting the US residential mortgage ra....

A mortgage rate, or mortgage interest rate, refers to the amount of interest a lender cha....Read More

Blog

Blog

Navigating overcapacity in China vis-à-vis US a....

China has been engulfed in overcapacity in industries recently, as also highlighted by US ....Read More

Like the way we think?

Next time we post something new, we'll send it to your inbox