|

| |

|

|

| |

“We’re facing a transformative economic landscape. Central banks are poised to maintain high interest rates, while growth and inflation diverge globally. An election super cycle looms amidst significant geopolitical risks, and disruptive technology and sustainability are reshaping industries. The resilience we’ve honed will be vital, as we confront growth volatility, higher capital costs and geopolitical instability. Strategic foresight and adaptability will be key in navigating this challenging environment.”

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

|

Global Markets

|

|

-

1 April: Turkey’s main opposition party claims big election victories in main cities.

-

9 April: Nasdaq rebounds, as Treasury yields retreat and gold hits a record high.

-

11 April: The European Central Bank keeps interest rates unchanged.

-

16 April: Vladimir Putin tells Israel to pull back from a catastrophic clash.

-

19 April: Nikkei surges on good corporate earnings.

-

20 April: The UK announces its slowest CPI growth in two and a half years.

-

26 April: The Japanese Yen hits a 25-year record high of 158.58 Yen/1 USD.

-

30 April: Annual inflation in the Eurozone stands at 2.4% in April, unchanged from the previous month.

-

30 April: Federal Open Market Committee April meeting begins.

|

| |

|

|

|

|

| |

|

|

|

Equity

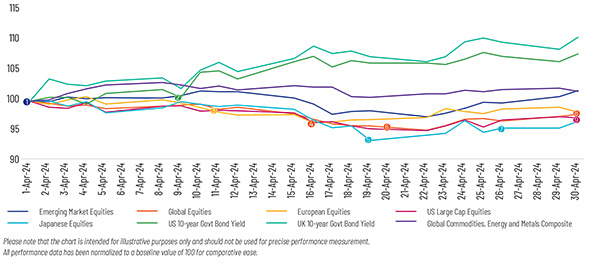

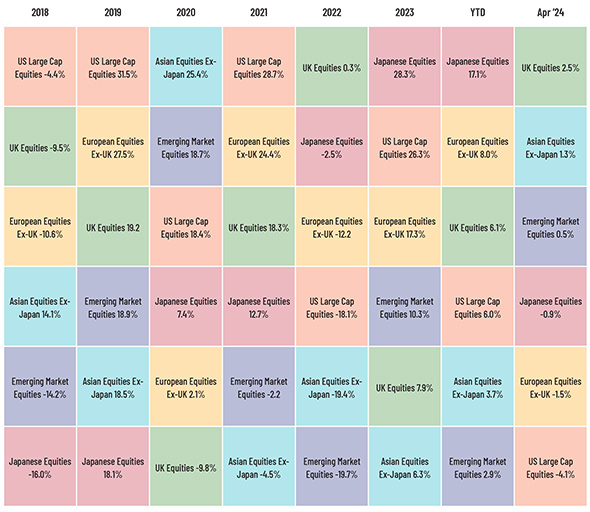

Global equity markets faced a downturn amid mixed signals from the US Federal Reserve (Fed), hinting at potential stagflation, alongside escalating tensions in the Middle East, particularly between Iran and Israel. Despite these tensions, the S&P 500 Index rebounded slightly amidst the busiest week of first-quarter earnings reporting, with earnings anticipated to have risen 3.7%, albeit failing to lift sentiment. The US housing market weakened, with existing home sales dropping and mortgage rates surpassing 7% for the first time since December. In the Eurozone, equities declined, as geopolitical tensions in the Middle East soured investor confidence despite inflation returning to targeted levels. Although Europe’s growth momentum improved, it lagged behind that of the US, prompting the European Central Bank (ECB) to cut rates ahead of the Fed.

In Japan, stock markets suffered losses during the month. The Bank of Japan abandoned its negative interest rate policy in a bid to combat deflation. Meanwhile, Japan’s Manufacturing PMI showed signs of improvement, although real wages continued to decline. Emerging markets experienced volatility, initially rising before reversing gains, owing to China’s economic growth report indicating potential downturns despite faster-than-expected expansion in the first quarter. Argentina’s central bank cut its benchmark interest rate to 70% to curb rampant inflation, while Turkey’s local elections yielded surprising results, affecting investor sentiment.

|

|

|

Fixed Income

In April, the Bloomberg US Aggregate Bond Index declined. Despite this drop, the Fed maintained its policy rates without any adjustments. However, market expectations regarding interest rate cuts shifted rapidly during this period. The Fed chose to keep interest rates steady for the sixth consecutive meeting in April. In terms of yields, the yield on the 10-year US Treasury note increased to 4.69% by the end of April. Simultaneously, the yield on its 2-year bond rose to 5.04%. Consequently, the 10-/2-year yield spread widened over the course of the month. Corporate investment-grade and high-yield bonds delivered slightly negative returns. Credit spreads modestly increased.

Eurozone government bond yields reached multi-month highs in April. Key economic indicators favoured the ECB’s restrictive monetary policy stance, with inflation remaining stable at 2.4%, while core inflation eased slightly to 2.7% from the previous month’s 2.9%. The Eurozone economy rebounded, with 0.3% QoQ growth in Q1 2024, with business activities, especially in the services industry, exhibiting signs of recovery. ECB President Christine Lagarde emphasised a data-dependent approach for future rate decisions.

|

|

|

|

|

Commodities

Overall, global commodity prices increased, driven by gains in metals and agricultural components. However, the energy sector made only a modest contribution to these returns. The surge in crude oil futures was partly offset by a decrease in natural gas prices, owing to low demand and excess supply in the US. The S&P GSCI Agriculture Index saw growth primarily on significant increases in tea and coffee futures, which were influenced by adverse climatic conditions in producer regions. Additionally, wheat futures rose, driven by unfavourable weather conditions and supply concerns from key producers. In the realm of industrial metals, copper futures led the way with substantial gains. Long-term demand for copper played a role, while the closure of the largest mine in Panama affected the supply chain. Furthermore, silver and gold futures rose significantly, as investors sought safe-haven assets amidst geopolitical tensions in the Middle East and uncertainty surrounding Fed rate cuts.

|

|

|

|

Central Bank Quotes

“Sustainable and stable achievement of our 2% inflation target is coming into sight. The possibility of achievement is expected to increasingly heighten.”

Kazuo Ueda, Governor, Bank of Japan

“We just need to build a bit more confidence in this disinflationary process, but, if it moves according to our expectations, if we don’t have a major shock in development, we are heading towards a moment where we have to moderate the restrictive monetary policy.”

Christine Lagarde, President, ECB

|

|

Market Indices

|

| |

|

|

|

In case you missed it

|

|

What’s Ahead

-

May 29,2024 – ECB Financial stability review meeting

-

June 6, 2024 – Eurozone – ECB monetary policy meeting

-

June 11, 2024 – UK – Unemployment Rate

-

June 12, 2024 – US – FOMC Meeting

-

June 14, 2024 – Japan – BoJ Interest Rate Decision

|

| |

|

|

| |

|

|

| |

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, analytics and technology solutions to the financial services sector, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 500 financial institutions and consulting companies to operate more efficiently and unlock their human capital, driving revenue higher and transforming operations. Acuity is headquartered in London and operates from 10 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, visit www.acuitykp.com

|

|

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com

|

|

|

|

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved.

|

|

|

|

|

|

|

|