|

| |

|

|

| |

“In August, market resilience in the face of political and economic headwinds affirmed the strength of diversified portfolios. The Federal Reserve’s readiness to cut rates in response to a slight rise in unemployment and recession indicators demonstrates a commitment to sustaining economic growth. Despite the uncertainty surrounding election outcomes, market confidence is buoyed by solid corporate earnings, particularly beyond the tech sector. A strategic mix of defensive equities and high-quality fixed income is advocated to navigate potential volatility. The anticipated Fed rate cuts have implications for the dollar, highlighting the need for dollar-hedged strategies and broader international diversification. While we monitor for a more assertive Fed policy in the event of further labor market softening, our stance remains one of cautious optimism, focusing on stability and seizing growth opportunities in a fluctuating market landscape.”

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

| |

|

|

|

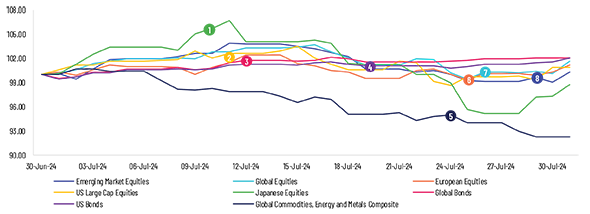

Global Markets

.jpg)

|

| |

|

|

|

-

August 5: The U.S. Treasury yield curve turned positive for the first time in two years, raising fears of an impending economic downturn. – US Bonds

- August 7: global investors moved funds into money market accounts due to market volatility in the US and a stronger yen. – Global Bonds

- August 14 – An unexpected rise in US crude inventories and worries about threatened supplies due to wider Middle East conflict dragged the oil prices lower – Global Commodities, Energy and Metals Composite

- August 19: Indian shares rebounded, with IT stocks leading the rally as solid US economic data eased concerns about a recession, boosting global risk appetite – Emerging market equities

- August 21: France’s PMI soared to a 27-month high, fueled by the Olympic Games, whereas Britain’s PMI rallied, indicating an uptick in business activity. – European equities

- August 22: Japan’s factory activity shrank in August amid subdued demand. – Japanese Equities

- August 23: Global stocks surged as investors poured money into equity funds, driven by hopes of a Fed rate cut in September. – Global Equities

- August 27: US consumer confidence rose, but concerns about the labour market are growing with unemployment at 4.3%. –US Large Cap equities

|

| |

|

|

|

|

| |

|

|

|

Equity

After the US Federal Reserve (Fed) gave the strongest indication yet that it would cut rates in September, global equity markets experienced a broad-based rally in August. Easing inflation and downside risks to the labour market prompted the Fed to consider slashing rates. US equities also bounced back after such developments, recovering from a sell-off that sparked volatility earlier in the month, due to recession worries and the reversal of yen carry trades. European stocks also reversed losses incurred earlier in the month to end in green on encouraging economic data and growing expectations of rate cuts by the Fed and the European Central Bank (ECB). Inflation in Europe fell to 2.2% in August from 2.6% in July, setting the stage for the ECB to lower rates next month. UK stocks rose following the Bank of England’s (BoE’s) decision to slash rates by 25bps to 5%. In Asia, Japanese stocks weakened, as core inflation accelerated to a four-month high of 2.4% in August, fortifying expectations of more rate hikes by the Bank of Japan in the approaching year. Japan’s annual inflation remained at 2.8% for a third consecutive month, with electricity prices peaking since March 1981. In China, markets saw a marginal uptick, despite continued macroeconomic weakness and deflationary concerns. Markets have been benefiting from the government’s efforts to push domestic real GDP towards 5% growth this year. To boost liquidity, the People’s Bank of China rolled out a CNY300bn one-year medium-term lending facility for banks, keeping the interest rate at 2.3% following a 20bp reduction in July. The Caixin General Manufacturing Purchasing Managers’ Index in the country edged up to 50.4 in August (vs 49.8 in July), aided by rising new orders and increased factory output.

|

|

|

Fixed Income

Fed chair, Jerome Powell, announced that interest rate cuts were on the cards. He expressed confidence that inflation remained well within the Fed’s target of 2% but warned that further cooling of the labour market may not bode well for the economy, endorsing a start to rate cuts. Meanwhile, annual core inflation increased to 2.6% in the 12 months through July, remaining unchanged from June. The unemployment rate increased to 4.3%, providing the necessary stimulus for a rate cut in September.

Following these developments, global bond markets witnessed growth with 10-year US Treasury yields hitting their lowest level since June 2023, falling 18bps to end August at 3.91%. Meanwhile, two-year US Treasury yields fell 38bps to also close the month at 3.91%. Consequently, the 10/2-year yield spread narrowed to zero. In general, Treasury yields fell across the board, and the US dollar weakened against all its developed-market counterparts.

In Europe, investors believe that the ECB would cut interest rates for a second time in its September meeting, with the odds increasing further as inflation softened in the region. 10-year German Bund yield fell to approximately 2.29% in August. 10-year UK gilt yield rose to 4.01% in the month, following cautious remarks from the BoE governor, George Bailey, about the future of interest rate cuts, which significantly reduced rate cut expectations by the BoE this month.

|

|

|

|

|

Commodities

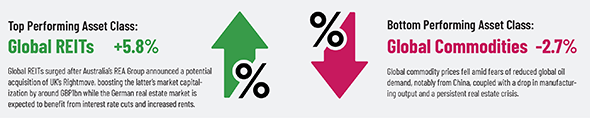

In August, global commodity markets saw negative returns, due mainly to falling energy prices. Oil prices dropped because of low demand. Speculation about OPEC+’s increasing production and diverse demand forecasts also kept oil prices muted. Meanwhile, iron ore prices hit a two-year low due to the real estate crisis in China. While natural gas prices rose on warmer weather in the US, ongoing geopolitical tensions in major gas-producing regions added uncertainty, influencing market sentiment. Gold prices increased as investors looked for safe assets owing to concerns surrounding inflation and geopolitical tensions. Silver prices also rose as the anticipation of interest rate cuts by the Fed made the precious metal more attractive. Industrial metals, especially copper, gained, as global copper ore shortage, along with increased demand for the metal, due to energy transition, boosted copper prices. Wheat futures rose on tightening global supplies, despite the availability of cheap Black Sea wheat. Canadian production increased but missed expectations, and European crops were damaged by heavy rains. Coffee and cocoa prices remained elevated thanks to a limited supply following a troubled growing season.

|

|

|

|

Central Bank Quotes

” It is important for monetary policy to stay the course in bringing inflation down towards its 4% medium-term target. Growth remains resilient, inflation has been trending downward and we have made progress in achieving price stability, but we have more distance to cover, ensuring price stability is important for sustainable growth”

Shaktikanta Das, Governor, Reserve Bank of India (8 August 2024)

“With regard to the outlook for inflation, participants judged that recent data had increased their confidence that inflation was moving sustainably toward 2%. Almost all participants observed that the factors that had contributed to recent disinflation would likely continue to put downward pressure on inflation in coming months.”

Jerome Powell, Chairman, Federal Reserve (21 August 2024)

|

|

Market Indices

.jpg)

|

| |

|

|

|

In case you missed it

|

|

What’s Ahead

-

September 14 – China: Unemployment Rate

-

September 17 – US: FOMC Meeting

-

September 18 – Great Britain: Inflation Rate YoY

-

September 20 – Eurozone: Consumer Confidence

-

September 23 – India: Manufacturing and Services PMI

-

September 26 – Japan: BOJ Monetary Policy Meeting

-

September 30 – Japan: Foreign Investments

|

| |

|

|

| |

|

|

| |

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, data management, analytics, talent, and technology solutions to the financial services industry, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 650 financial institutions and consulting companies to operate more efficiently and unlock their human capital and transforming operations. Acuity is headquartered in London and operates from 16 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, visit www.acuitykp.com

|

|

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com

|

|

|

|

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved.

|

|

|

|

|

|

|

|