|

|

| |

|

|

| |

The year 2025 commenced with some significant disruptions in the global equity market. Within the AI sector, the introduction of DeepSeek AI and the Chinese company’s announcement of a low-cost development strategy resulted in a substantial loss of market capitalisation in a single day in January. While AI holds immense potential for future growth, competition to lead in this space is intensifying rapidly. Additionally, the US president’s stance on tariffs on imports from certain countries triggered another major correction in equity markets, particularly in Asia. This is largely in line with what I mentioned in the last edition, and with further domestic and international policy changes expected under the new administration, continued volatility should be expected in the major asset classes and geographies. Investors would do well to adopt a strategic, diversified approach to navigate the coming months.

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

|

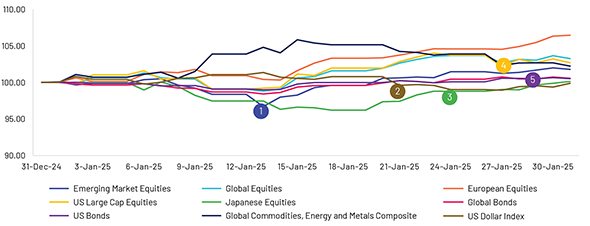

Global Markets

|

|

-

1. January 13: Indian shares plunged, with the mid-cap index seeing its steepest drop in seven months due to a strong US jobs report hinting at fewer Fed rate cuts and concerns over domestic earnings. – Emerging Market Equities

- 2. January 21: The GBP tumbled against a resurgent USD amid market jitters over potential new tariffs from the Trump administration. – US Dollar Index

- 3. January 24: Japan’s central bank has hiked interest rate to a 17-year high, responding to a surge in consumer prices seen in December. – Japanese Equities

- 4. January 27: Nvidia faced a historic $600 billion market-cap drop, driven by fears of rising competition from Chinese AI lab DeepSeek, marking the largest single-day loss ever for any US company. – US Large Cap Equities

- 5. January 29: The Fed kept interest rates steady, with Chair Jerome Powell stating that rate cuts will wait until inflation and job data justify them. – US Bonds

|

| |

|

|

|

|

| |

|

|

|

Equity

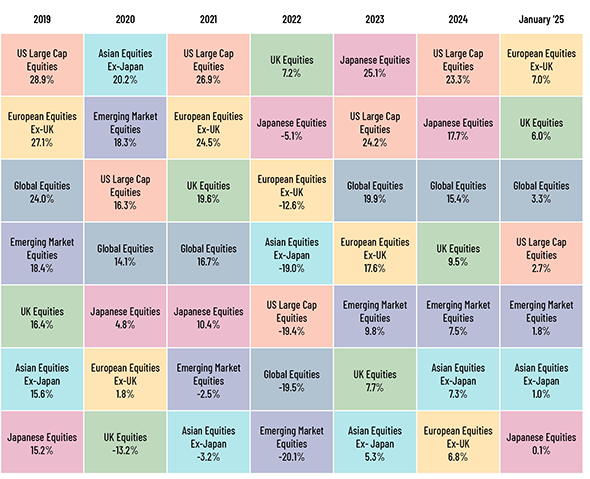

Global equity markets advanced in January, driven by a record rally in European shares, easing concerns about US tariffs on China and prospects of further monetary easing. However, rising oil prices and volatility in artificial intelligence (AI)-related stocks weighed on investor sentiment. US equities gained on strong corporate earnings and reassurances from major tech firms regarding continued AI investments. However, AI-related stocks faced pressure after China unveiled a competitive AI model with significantly lower funding. The Federal Reserve kept the fed funds rate steady at 4.25%-4.50%, pausing its rate-cutting cycle to assess progress in inflation. While economic activity remained solid and unemployment stable, the Fed acknowledged persistent inflation risks and an uncertain economic outlook.

European stocks surged, supported by falling bond yields, a European Central Bank (ECB) rate cut, strong corporate earnings, particularly in luxury goods and semiconductors, improved consumer confidence and relief over the absence of immediate US tariffs. The ECB lowered the key interest rate by 25 bps, citing an improved inflation outlook, but maintained a cautious, data-driven approach. Meanwhile, the UK’s stock index reached record highs, benefiting from expectations of further rate cuts and gains in the technology and financial sectors, amid AI-related concerns. In Asia, Japanese equities declined due to weakness in tech stocks and speculation over a Bank of Japan (BoJ) rate hike. The BoJ raised its key interest rate by 25 bps to 0.50%, the highest in 17 years, signalling further tightening. Chinese equities fell on concerns of US sanctions and trade uncertainties, although some gains were supported by surging exports, AI developments and regulatory pledges for market stability. The People’s Bank of China (PBoC) kept rates unchanged, focusing on stability in the yuan and economic growth, as GDP expanded by 5.4% in Q4 2024.

|

|

|

Fixed Income

In January 2025, global bonds saw positive performance due to a confluence of factors. Positive economic data from major economies, such as robust employment figures and stable growth indicators, enhanced investor confidence. Stable inflation rates also helped keep fixed income investments attractive. Additionally, there was a shift towards safer assets amid volatility in equity markets, driven by developments in the tech sector, as a new AI program from China’s DeepSeek caused risk assets to weaken and Treasury yields to decline. Performance was positive across various sectors, including Treasuries, mortgage-backed securities (MBS), investment grade and high yield corporates, senior loans, and emerging markets. Emerging markets, and corporates outperformed similar-duration Treasuries. The USD, which tends to be a headwind for emerging markets when it is strengthening, looks to be appreciating in response to tariff news. The municipal bond remained strong, driven by the combination of strong fund inflows and a favourable supply-demand dynamic, which supported municipal bond prices and yields. US Treasury yields also moved modestly lower amid calmer tariff rhetoric and steady Fed policy.

The yield spread between the US 10-year and 2-year Treasuries widened slightly due to manufacturing growth and expectations of further Fed rate cuts. Credit spreads narrowed slightly due to increased corporate bond trading, driven by improved corporate earnings. High yield bonds outperformed global investment grade and sovereign bonds in January. The Fed kept rates steady to manage inflation amid potential Trump tariffs. Meanwhile, the ECB cut the interest rate by 25 bps to 2.75% and hinted at further easing to stimulate economic growth.

|

|

|

|

Commodities

Precious metals surged to fresh record highs last month as President Trump extended his threats of trade tariffs on China, the European Union (EU), Canada and Mexico and pushed up demand for safe-haven assets. LME copper prices rose by more than 3% MoM in January, primarily due to early signs of demand recovery in China as copper cathode inventories fell while premiums for both imported and domestic cargoes increased. Meanwhile, the prospects of a prolonged trade war could trigger bigger stimulus announcements from China, limiting the downside to copper prices. As for aluminium, 3M prices trading at LME rose by almost 2% MoM last month, following the reports of the EU proposing a phased ban on imports of Russian aluminium to the bloc. In agri commodities, corn prices rallied over 5% MoM in January as recent official estimates indicated an output loss from key producing nations such as the US, Argentina, Brazil, and Ukraine. Crude oil traded volatile last month as uncertainty over US import tariffs on Canadian and Mexican energy supplies keeps traders anxious. US natural gas turned out to be the biggest loser in the commodity complex, with front-month Henry Hub futures falling by more than 16% MoM in January as predictions of warmer weather in the US weighed heavily on the heating demand.

|

| |

|

|

|

Foreign Exchange

The USD’s predominance, underpinned by global trade uncertainties, was the core theme in January. The Fed’s FOMC meeting signalled a somewhat hawkish tone, and with rates on hold, the USD remained firm. President Trump’s announcement of his plans to impose tariffs on a number of countries and commodities led to further USD strengthening. The JPY withstood some of the pressure after the BoJ raised policy rates to a historical high. The EURUSD pair continued its downward trajectory, capitulating to the Fed’s decision to hold interest rates, the ECB’s rate cut and a weak GDP print in Q4 2024. The Pound sterling depreciated against the USD, propelled by rather domestic factors –a slowing economy and expectations of a rate cut in February.

In Asia, the INR slid to a record low, driven by tariff fears and significant FII outflows; the Reserve Bank of India’s (RBI’s) intervention (liquidity injection) could manage INR volatility to some extent. The CNY remained relatively stable, as the central bank implemented measures to stabilize the CNY amid rising USD demand. Elsewhere, the Colombian Peso sold off as President Trump imposed a 25% tariff on all imports. Consequently, both the Mexican peso and the Canadian dollar fell to multi-year lows in reaction to heightened concerns of tariff imposition.

|

| |

|

|

|

Economic Outlook

Global growth is expected to remain steady but below historical averages, mainly due to positive adjustments in the United States balancing out declines in other major economies. Inflation rates are anticipated to decrease, reaching target levels sooner in advanced economies compared to emerging markets.

Medium-term risks are more likely to be negative, while the short-term outlook presents mixed risks. Positive factors could boost growth in the United States in the near term, whereas other countries face challenges due to high policy uncertainty. Policy changes could disrupt the ongoing reduction in inflation, potentially impacting fiscal and financial stability. Addressing these risks requires a focused policy approach that balances inflation control with economic activity, rebuilds financial buffers, and enhances medium-term growth through structural reforms and stronger international cooperation.

|

| |

|

|

|

Central Bank Quotes

“In support of our goals, today the Federal Open Market Committee decided to leave our policy interest rate unchanged and to continue to reduce our securities holdings. I will have more to say about monetary policy after briefly reviewing economic developments. Recent indicators suggest that economic activity has continued to expand at a solid pace. For 2024 as a whole, GDP looks to have risen above 2 percent, bolstered by resilient consumer spending. Investment in equipment and intangibles appears to have slowed in the fourth quarter but was strong for the year overall. Following weakness in the middle of last year, activity in the housing sector seems to have stabilized.”

Jerome Powell, Chairman, Federal Reserve (29 January 2025)

” The disinflation process is well on track. Inflation has continued to develop broadly in line with the staff projections and is set to return to the Governing Council’s 2% medium-term target in the course of this year. Most measures of underlying inflation suggest that inflation will settle at around the target on a sustained basis. Domestic inflation remains high, mostly because wages and prices in certain sectors are still adjusting to the past inflation surge with a substantial delay. But wage growth is moderating as expected, and profits are partially buffering the impact on inflation”

Christine Lagarde, President of the European Central Bank (30 January 2025)

|

|

Market Indices

|

| |

|

|

|

In case you missed it

-

Ready to uncover how corporate bankruptcies in the U.S. are skyrocketing, with no signs of slowing down? – August 2024

Corporate America: On a Bankruptcy Boom | Acuity Knowledge Partners

-

Discover how autonomous mobility is revolutionizing safety with driverless vehicles, demanding bold investments and groundbreaking research! – August 2024

Autonomous Mobility: The Road to a Driverless Future | Acuity Knowledge Partners

-

Explore the latest trends and opportunities in SME lending, highlighting digital transformation, cross-border financing, and supportive regulatory policies? – August 2024

New Trends and Opportunities in SME Lending: What you need to know | Acuity Knowledge Partners

-

Learn how automation is transforming credit risk monitoring, driving unparalleled efficiency and precision in the financial sector — read on to discover powerful solutions – August 2024

Automation’s Impact on Credit Risk Monitoring | Acuity Knowledge Partners

|

| |

|

What’s Ahead

-

February 15, 2025 – South Korea: Unemployment rate

-

February 17, 2025 – Japan: Industrial Production MoM

-

February 18, 2025 – Australia: RBA Interest Rate Decision

-

February 20, 2025 – Argentina: Consumer Confidence

-

February 23, 2025 – Germany: Federal Election

-

February 28, 2025 – India: GDP Growth Rate YoY

-

March 1, 2025 – Mexico: Fiscal Balance

-

March 3, 2025 – China: Caixin Manufacturing PMI

-

March 5, 2025 – Euro Area: ECB monetary policy meeting

-

March 6, 2025 – Brazil: Balance of Trade

|

|

|

| |

|

|

| |

|

|

|