|

|

| |

|

|

| |

We’ve seen a strategic shift toward small-cap stocks amid weaker US inflation and labor data, demonstrating the market’s adaptability to economic signals. Although small caps have performed significantly better, investors should proceed with caution. In the absence of a recession, the market’s expectation for Federal Reserve rate cuts may be overly optimistic. Moving forward, a judicious approach is essential. Diversification is advisable, with the UK and Europe offering attractive prospects against the unpredictability of the US markets. As we navigate this period, it’s crucial to balance the current enthusiasm for small-cap stocks with a broader investment strategy. This approach will help maintain resilience in the face of potential over-optimism regarding the market’s expectations for rate cuts.

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

|

Global Markets

|

|

-

July 10: Overseas investors bought Japanese stocks worth a net JPY 916.05 bn in a week.

- July 11: U.S. equity faced its first weekly outflow as caution and profit-taking took hold.

- July 12: Global debt funds attracted inflows on expectations of a Fed rate cut amid weakening labor market conditions and easing inflation.

- July 19: US bond managers are steering clear of long-term government bonds as they expect fiscal worries to spur periodic volatility.

- July 24: Oil prices slipped as investors focused on the prospect of swelling oil supplies and weak demand.

- July 25: European stocks tumbled after underwhelming reports from Kering and Nestle SA.

- July 26: Global equity market dropped due to a slump in global tech stocks.

- July 29: China’s factory activity shrank as a protracted property crisis and job insecurity drag on growth in emerging markets.

|

| |

|

|

|

|

| |

|

|

|

Equity

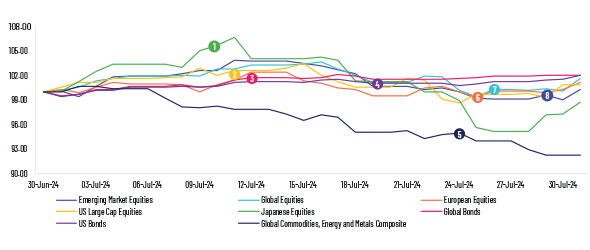

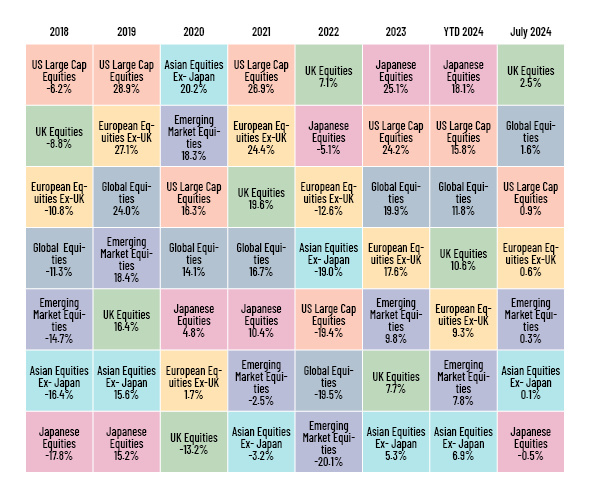

Global equity markets ended in the green in July, buoyed by a last-minute rally after the US Federal Reserve signaled its readiness to cut rates in September should inflation continue its steady decline. US equities advanced on upbeat economic data, falling unemployment levels, and anticipation of rate cuts by the Fed in September. Latest data revealed US GDP growth for the second quarter was higher than anticipated, set against a backdrop of decreasing inflation. European stocks ended higher, boosted by strong corporate earnings and Joe Biden’s sudden withdrawal from the US presidential race. In response to ongoing concerns about inflation, the European Central Bank maintained steady interest rates. Inflation held steady at the Bank of England’s (BoE) target of 2% – a development that may nudge the central bank to slash rates next month. Elsewhere Japan’s stock market rose by 5.8% as the yen hit a four-month high, following the Bank of Japan’s (BoJ) first interest rate hike in 15 years. The key short-term interest rate was raised to 0.25%, signaling a shift in monetary policy, which included a reduction in monthly bond buying and a lowering of the BoJ’s balance sheet. Moving to China, markets were weighed down by its persistent property sector crisis, burgeoning local government debts, and escalating trade tensions with the US. China’s consumer price index weakened over the month amid weak demand. The People’s Bank of China cut its lending rate for one-year medium-term policy loans by 20bps – the biggest rate cut since 2020 – in a bid to boost its slowing economy.

|

|

|

Fixed Income

Global bond markets witnessed an uptick in July, with US 10-year Treasury yields falling on slowing manufacturing activity and weakening consumer confidence. The yield curve steepened, causing the difference between 10-year and 2-year US Treasury yields to narrow to around negative 20bps, marking the smallest gap in yields since January 2024. The yield on 2-year US Treasuries fell 42bps to 4.29% and 10-year US Treasuries shed 27bps to end at 4.09%. Amidst this, uncertainty persisted over the timing of the Fed’s anticipated rate cuts, leading investors to gravitate towards more secure investments, especially as default rates in high-yield bonds rose.

In Europe, the yield on the 10-year German bund fell to approximately 2.29%. Investors remained cautious, awaiting further economic indicators and clarity on the European Central Bank’s policy direction amidst stagnant Eurozone manufacturing activity. The yield on the 10-year UK gilts declined as investors increasingly anticipated the BoE to cut interest rates due to concerns about a potential recession in the United States.

|

|

|

|

Commodities

The global commodity markets posted negative returns in July, as energy and metal prices declined. Oil prices softened significantly, due to geopolitical tensions and weakening Chinese consumption. Demand concerns and geopolitical tensions added to downward pressure on oil prices. On natural gas, prices melted down in the US summer heat, considered unusual at the height of the air-conditioning season, when a lot of gas is burned to generate electricity, due to higher storage in Europe on milder winter demand. Additionally, demand for natural gas fell in Southeast Asia amid cool weather. In precious metals, gold prices edged higher due to concerns over the global economic slowdown while silver prices fell amid sell-offs for profit-making, strong US GDP data, and the uncertainty about interest rate cuts. Industrial metals lost ground, too, particularly due to a decrease in copper prices for a second consecutive month, owing to continued weakness in China’s housing sector along with growing inventories. Wheat futures fell due to a significant increase in production amid a recovery of Ukrainian and Russian wheat exports during the period. However, coffee and cocoa prices remained elevated on tight supplies following a troubled growing season.

|

| |

|

|

|

Central Bank Quotes

“What we’ve said is that we didn’t think it would be appropriate to begin to loosen policy until we had greater confidence, that inflation was returning sustainably to 2%. I would say that we didn’t gain any additional confidence in the first quarter, but the three readings in the second quarter do add somewhat to confidence.”

Jerome Powell, Chairman, Federal Reserve

” Risks to growth were “tilted to the downside and bank would not pre-commit to any rate path and data would guide decisions. So, the question of September and what we do in September is wide open, and there was now a strong likelihood the dialing back of monetary policy was underway.”

Christine Lagarde, President, European Central Bank

|

|

Market Indices

|

| |

|

|

|

In case you missed it

|

| |

|

What’s Ahead

-

August 19, 2024 –Spain: Consumer Confidence

-

August 21, 2024 – India: M2 Money Supply

-

August 22, 2024– Japan: Manufacturing and Services PMI

-

August 29, 2024 – US: GDP Growth Rate QoQ

-

August 30, 2024 – US: Fed Balance Sheet

|

|

|

| |

|

|

| |

|

|

| |

|

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, analytics and technology solutions to the financial services sector, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 500 financial institutions and consulting companies to operate more efficiently and unlock their human capital, driving revenue higher and transforming operations. Acuity is headquartered in London and operates from 10 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, visit www.acuitykp.com

|

|

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com

|

|

|

|

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved.

|

|

|

|

|

|

|