|

| |

|

|

| |

“As we reflect on the past quarter, the standout narrative has been the impressive resilience of growth stocks, particularly within the technology sector. Despite broader market uncertainties and inflationary pressures, tech companies, especially those in artificial intelligence, have outperformed, delivering substantial returns. This underscores the sector’s robustness and its critical role in driving forward economic growth. We remain attentive to the evolving market dynamics and central bank policies, yet we are encouraged by the tech sector’s potential to offer investors a harbour of growth amidst market volatility. Looking ahead, strategic investments in the AI and tech sectors remain a key focus for sustained performance.”

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

| |

|

|

|

Global Markets

|

| |

|

|

|

-

June 2: OPEC+ decides to prolong significant oil production reductions until 2025.

- June 6: European stocks rise after ECB cuts rates for first time in 5 years.

- June 9: Modi sworn in as India’s Prime Minister for the third term, faces coalition hurdles.

- June 11: Federal Reserve holds rates steady for seventh time, projects single cut this year.

- June 14: G7 addresses concerns regarding China’s trade practices.

- June 19: Nvidia overshadows Microsoft as the world’s most valuable company.

- June 24: India’s overseas gold reserves hit a 6-year low, making up 47% of the total.

- June 25: Argentina undergoes a technical recession as job losses ascend under Milei.

- June 26: US dollar at 38-year high against Japanese yen.

|

| |

|

|

|

|

| |

|

|

|

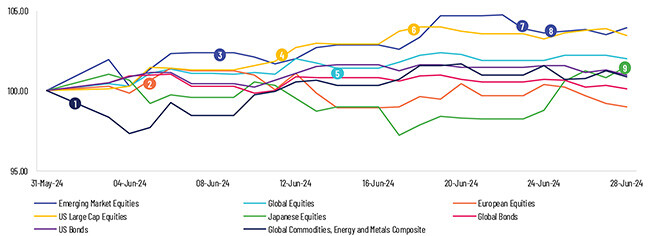

Equity

Global equity markets rose in June after the European Central Bank (ECB) cut rates for the first time in five years. Denmark’s central bank followed suit, lowering its benchmark interest rate. In the US, markets improved on slowing inflation and the unemployment rate rose to 4%, raising investor hopes for rate cuts. However, European stocks fell amid political uncertainty following the recent elections in the European Union. The risks posed by this uncertainty dented market gains realized after the ECB’s rate cut earlier in the month. Meanwhile, the Bank of England (BoE) kept its key interest rate steady at 5.25% as inflation fell to the central bank’s target of 2%. In Japan, stock prices increased as the Bank of Japan (BoJ) maintained its interest rates and signaled an imminent reduction in bond purchases. However, investors remain cautious as the BoJ is expected to unveil its tapering plan, set to begin in August. Chinese shares also slipped as domestic investors grew more wary about the country’s growth outlook. Furthermore, the long-running property downturn continued to dampen the risk appetite of investors. The economy was affected by a faltering property sector and new trade sanctions from the US and UK, particularly affecting the electric vehicle industry. Despite the headwinds, some economic indicators hinted at resilience. The most recent manufacturing, trade, and inflation data pointed to nascent signs of improvement.

|

|

|

Fixed Income

Global bonds rose marginally in June on signs that inflation was easing around the world. The Federal Reserve (Fed), in its June meeting, decided to hold policy rates steady at 5.25-5.50% for the seventh consecutive time, stating it would be in a position to cut rates only after ascertaining that inflation was moving sustainably toward the target rate. Markets anticipate only one rate cut this year. The yield on the 10-year US Treasury note dropped to 4.39% by the end of June as investors awaited further developments to gauge the Fed’s monetary policy outlook. Simultaneously, the yield on its 2-year bond decreased to 4.77%. Consequently, the 10-2-year yield spread narrowed over the month.

Global bonds rose marginally in June on signs that inflation was easing around the world. The Federal Reserve (Fed), in its June meeting, decided to hold policy rates steady at 5.25-5.50% for the seventh consecutive time, stating it would be in a position to cut rates only after ascertaining that inflation was moving sustainably toward the target rate. Markets anticipate only one rate cut this year. The yield on the 10-year US Treasury note dropped to 4.39% by the end of June as investors awaited further developments to gauge the Fed’s monetary policy outlook. Simultaneously, the yield on its 2-year bond decreased to 4.77%. Consequently, the 10-2-year yield spread narrowed over the month.

Yields on eurozone government bonds declined in June as the ECB reduced interest rates by 25 basis points during its June meeting. This move came after nine months of stable rates, driven by inflation trends. However, domestic price pressures remain elevated relative to the ECB’s target rate of 2%, and the ECB continues to maintain a data-dependent approach.

|

|

|

|

|

Commodities

Global commodity markets gained in June as energy prices remained elevated. Oil prices edged higher due to the increase in demand expected during the summer and OPEC+ production restraints. The ongoing tensions in the Middle East and Ukraine’s drone attacks on Russian oil infrastructure have also supported oil prices. Precious metals are under pressure amid uncertainty about interest rate cuts. Gold and silver prices fell due to caution ahead of US inflation data and the strengthening of the US dollar following robust US business activity data. Industrial metals also lost ground, particularly due to the decrease in copper prices amid weak demand from China – the top consumer of copper. Wheat futures were under pressure from an advancing US harvest. Coffee and cocoa prices remained elevated due to tight supply following a troubled growing season.

|

|

|

|

Central Bank Quotes

“These dynamics can continue as long as they continue, we’ve got a good strong labour market. We think we’ve been making progress toward the price stability goal. We’re asking … is our policy stance about right? And we think yes, it’s about right.”

Jerome Powell, Chairman, Federal Reserve

“Price stability goes hand in hand with financial stability. We pay close attention to the smooth functioning of financial markets, and today we continue to do so.”

Christine Lagarde, President, European Central Bank

|

|

Market Indices

|

| |

|

|

|

In case you missed it

|

|

What’s Ahead

-

July 9 – US Consumer Credit

-

July 17 – Euro Area Inflation Rate MoM

-

July 18 – ECB: Monetary policy meeting in Frankfurt

-

July 30 – US FOMC Meeting

-

August 1 – BoE Interest Rate Decision

-

August 2 – US Unemployment Rate

|

| |

|

|

| |

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, analytics and technology solutions to the financial services sector, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 500 financial institutions and consulting companies to operate more efficiently and unlock their human capital, driving revenue higher and transforming operations. Acuity is headquartered in London and operates from 10 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, visit www.acuitykp.com

|

|

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com

|

|

|

|

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved.

|

|

|

|

|

|

|

|