|

| |

|

|

| |

“In this edition, we spotlight the robust performance of global equity markets, with US tech leading a notable surge and European stocks climbing amid central bank caution. Emerging markets showed positive, albeit slower, growth. Despite an inverted yield curve, the fixed income asset class fared positively in May. Commodities trade was a tale of contrasts; energy retreated, and agricultural commodities thrived on supply concerns. Metals such as gold and silver performed strongly. To capitalize on the evolving economic landscape, navigating these complex market conditions with astute strategic insights is crucial, ensuring the full potential of emerging opportunities is harnessed while mitigating risks.”

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

|

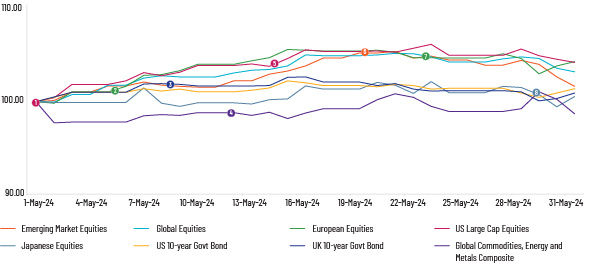

Global Markets

|

|

-

1 May: US Federal Reserve holds benchmark lending rate at a 23-year high in a range of 5.25-5.5% (US Large Cap Equities).

- 6 May: Eurozone bond yields hit multi-week lows (European equities)

- 9 May: Bank of England maintains key lending rate at 5.25%, the highest since 2008 (UK 10-year Govt Bond Yield).

- 12 May: Brent crude oil prices drop for the fourth consecutive week to USD74.17 (Global Commodities, Energy and Metals Composite).

- 15 May: US Core CPI cools for the first time in 6 months (US Large Cap Equities).

- 20 May: The People’s Bank of China keeps the one-year loan prime rate unchanged at 3.45% (Emerging Market Equities).

- 23 May: The UK Consumer Price Index (CPI) drops to 2.3%, the lowest in three years (European Equities).

- 29 May: Japan’s stock market index hits the highest level since July 1990 (Japanese Equities).

|

| |

|

|

|

|

| |

|

|

|

Equity

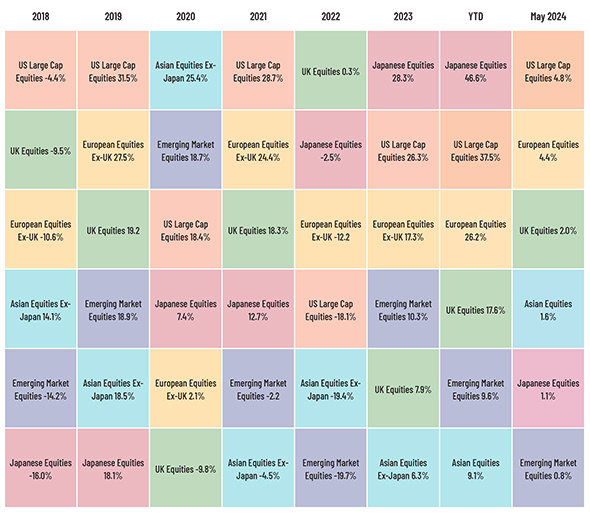

Global equity markets experienced a marked upswing, bolstered by AI trade advancements and solid corporate earnings reports. US stocks enjoyed a particularly strong period, with the technology sector’s impressive financial results leading the charge. Highlighting this trend, Nvidia’s ascent briefly pushed the tech-heavy index to reach a new high as the month ended.

All major indices reached record highs as the US CPI announcement in April was aligned with expectations, signalling an end to the three months of elevated inflation. European equities also had a strong month, reaching record highs. However, momentum slowed in the latter half of the month, following cautious remarks from the European Central Bank (ECB), which tempered expectations for rate cuts. Headline inflation in the region remained stable in April, and while manufacturing activity continued to decline, the downturn showed signs of moderation. The Bank of England (BoE) maintained its benchmark interest rate as predicted by the market.

Emerging market equities posted gains, although trailing behind developed markets in May. Chinese equities experienced a boost in the first half of the month due to strong holiday spending and the government’s stimulus package for the property sector. However, trade tensions with the US and concerns over military exercises near Taiwan tempered the advances later in the month. The People’s Bank of China (PBoC) maintained its one-year medium-term lending facility rate. Indian equities saw slightly positive returns in May. The Reserve Bank of India (RBI) approved a record surplus transfer of INR2.11tn to the government for the fiscal year that ended in March, surpassing analysts’ expectations.

Despite closing with gains, Japanese stocks exhibited signs of weakness amid ongoing worries about slow economic expansion and lacklustre consumer expenditure. The governor of the Bank of Japan (BoJ) emphasised the importance of resetting inflation expectations and the difficulty in determining a neutral interest rate, given the prolonged period of near-zero short-term interest rates over the past three decades.

|

|

|

Fixed Income

In May, global bonds appreciated amid growing speculation of rate cuts in the second half of the year. In the same period, the yield on the 10-year US Treasury note declined significantly, to 4.51% from 4.64%. The yield on its 2-year bond declined marginally, to 4.89% from 4.94%. The 10-year versus 2-year Treasury yield curve remained inverted as investors continued to weigh in the risk of recession. Inflation rates aligned with market predictions, suggesting potential rate cuts by the US Federal Reserve (Fed) later in the year. At its May meeting, the Fed held the federal funds target rate steady at 5.25-5.5%, marking the sixth consecutive pause. Fed Chair Jerome Powell pointed to persistent inflation in the first quarter, indicating a protracted journey towards the 2% inflation target. Powell affirmed that the current policy stance is appropriately restrictive and suggested that a rate hike is not imminent. Despite tighter credit conditions, riskier corporate and high-yield bonds have outperformed sovereign bonds. Specifically, investment-grade bonds’ yield premium fell, while high-yield bonds’ premium dropped relatively sharply.

In the Eurozone, government bond yields hovered around multi-month highs. Based on low consumer inflation and positive economic growth, European investors expect rate cuts in September. Core inflation in the region rose to 2.9% in May, as did consumer prices to 2.6%.

In Asia, domestic bond markets posted positive returns across the region, despite fluctuations in US Treasuries. Inflation rates in major Asian countries, including Indonesia, South Korea, and Taiwan, came in below expectations, signaling a disinflationary trend. In China, manufacturing activity shrank unexpectedly in May, and growth in the services sector also decelerated. On the monetary policy front, the PBoC held its one- and five-year loan prime rates steady at 3.45% and 3.95%, respectively, in May.

|

|

|

|

Commodities

Global commodities underwent a period of overall decline, but they also saw gains in performance, marked by divergent trends across distinct sectors. The energy sector suffered the steepest decline, in contrast to agricultural commodities and metals, which registered the most substantial gains.

The energy sector’s overall performance was negatively impacted by the decrease in global demand, which led to a drop in Brent crude oil prices. Production cuts announced by OPEC+ nations did little to help overall prices. On the other hand, demand for natural gas in the US surged due to heightened power needs during the summer, somewhat mitigating the overall negative impact on the energy sector. Iron ore prices declined in May due to a deteriorating demand outlook in China, exacerbated by PMI reports indicating contraction. Reduced steel production and high inventory levels further pressured prices.

Agricultural commodities delivered strong returns, with wheat futures leading the way. Demand for wheat increased against a backdrop of reduced supply caused by adverse weather conditions in key producing regions, particularly Russia. Soybeans also saw price increases due to supply disruptions due to flooding and heavy rains in other major production areas.

The current landscape is complex, with volatile commodity prices, driven by geopolitical tensions and fluctuations in demand and economic indicators. While gold and silver have performed strongly, industrial metals present a mixed picture, reflecting the broader uncertainties in global markets.

|

| |

|

|

|

Central Bank Quotes

“In the absence of a significant weakening in the labor market, I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy.”

Christopher Waller, Fed Governor

“The risk of undershooting the inflation target and eventually having to pay too high a price in terms of declining activity was now seen as being at least as high as the risk of acting too early and overshooting the target over the medium term”

ECB Monetary Policy Meeting minutes

|

|

Market Indices

|

| |

|

|

|

In case you missed it

|

| |

|

What’s Ahead

-

June 20, 2024 – Japan – Foreign Bond Investment

- June 20, 2024 – Eurozone – ECB General Council Meeting

- June 21, 2024 – Japan – Inflation Rate YoY

- June 21, 2024 – UK Manufacturing PMI

- June 25, 2024 – US – Consumer Confidence

- June 25, 2024 – Spain – GDP Growth Rate

-

June 28, 2024 – US – Personal Income M/M

|

|

|

| |

|

|

| |

|

|

|

| |

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, analytics and technology solutions to the financial services sector, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 500 financial institutions and consulting companies to operate more efficiently and unlock their human capital, driving revenue higher and transforming operations. Acuity is headquartered in London and operates from 10 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, visit www.acuitykp.com

|

|

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com

|

|

|

|

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved.

|

|

|

|

|

|

|