|

| |

|

|

| |

“The recent shift in policy by the Federal Reserve, in response to low inflation, has boosted confidence in both stock and bond markets, improving the outlook for diversified investment portfolios. However, the upcoming US elections add an element of uncertainty that could unsettle this positive trend. While the central bank’s interest rate cuts have created a supportive environment, the possibility of election-related volatility looms, indicating that investors should approach the market with caution. Finding the right balance between the Fed’s accommodating stance and the uncertainties surrounding the political outcome will be crucial in shaping the investment landscape. It’s a time for strategic flexibility, as the interaction between policy and politics will undoubtedly impact market direction and stability in the near future.”

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

|

Global Markets

|

| |

|

|

|

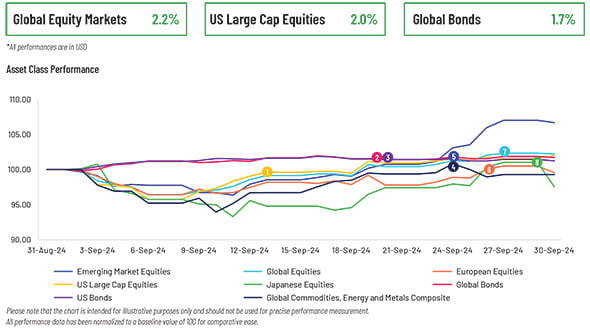

- September 13: The equity market outperformed, led by rate-sensitive small cap stocks, as hopes of the 50bps Fed rate cut boosted investor sentiment. – US Large Cap Equities

- September 20: Global bond funds continued to attract inflows for the 39th consecutive week, alongside an outperformance in short-term and high-yield bond funds led to moderate investor withdrawals. – Global Bonds

- September 20: Treasury yields rose as the start of the Federal Reserve’s first rate-cutting cycle in more than four years whet investors’ risk appetite. – US Bonds

- September 24 – China introduced stimulus measures to support its economy and stock markets, leading to a rise in commodity prices due to anticipated improvements in demand. – Global Commodities, Energy and Metals Composite

- September 24: China’s central bank launched its largest stimulus since the pandemic to combat deflation and meet growth targets – Emerging Market Equities

- September 26: European stocks, particularly those exposed to China such as luxury and mining stocks, hit a record high after the Chinese government announced stimulus measures to boost its ailing economy. – European Equities

-

September 27: Global stock indices hit record highs after chipmaker Micron Technology’s positive forecast, while interest rate cuts by major central banks lifted investment interest in precious metals. – Global Equities

- September 29: Japanese stocks tumbled after the governing party chose Shigeru Ishiba, a critic of the country’s longstanding ultralow interest rates, as its leader. – Japanese Equities

|

| |

|

|

|

|

| |

|

|

|

Equity

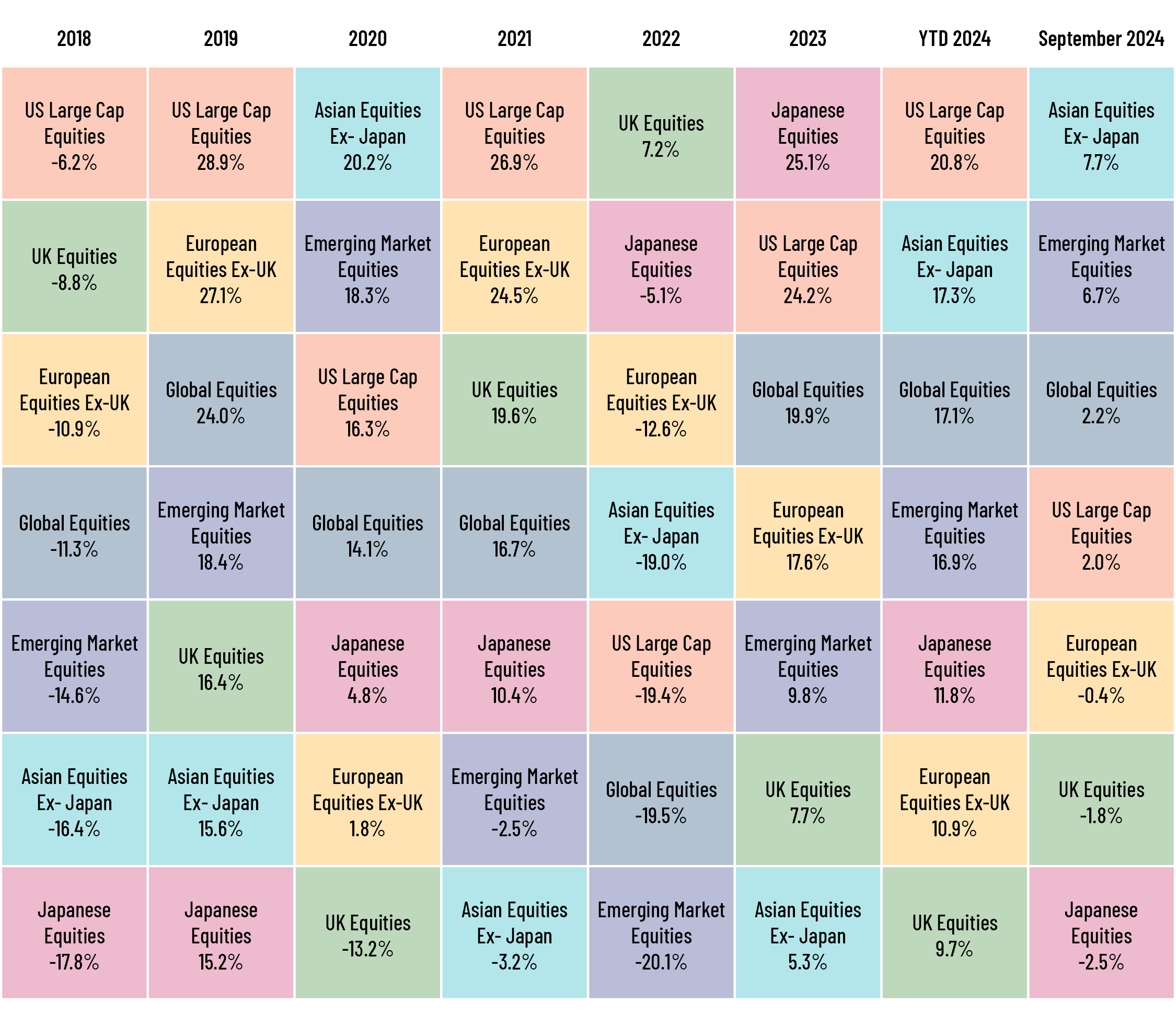

Equity markets rallied following the US Federal Reserve’s (Fed’s) highly anticipated rate cut after holding steady for more than a year. A cooling labour market and softening inflation encouraged the Fed to cut rates. US equities also advanced because of the Fed’s rate cut. Meanwhile, the US’s core personal consumption expenditure gauge at 2.2% in August, lower than expected, giving investors hope of a second rate cut in November. In Europe, markets rose on the Fed’s rate cut and China’s stimulus measures. The European Central Bank (ECB) also eased rates to stimulate growth, while inflation is back close to its 2% target. Inflation in eurozone eased to 1.8%, below its target in September. UK stocks eked out gains following the Bank of England’s (BoE’s) decision to leave rates unchanged at 5%. The UK’s headline inflation remained unchanged at 2.2% in August, lingering only slightly above the BoE’s 2% target. In Asia, Japanese stocks weakened amid rising inflation and a strengthening yen. The Bank of Japan left rates unchanged at its September meeting. The apex bank stated that the country’s economy was growing in line with expectations while rising wages were boosting domestic consumption, keeping inflation on track to meet its 2% target. In China, markets rallied after the Chinese government announced a slew of stimulus measures to shore up its ailing economy. The People’s Bank of China (PBoC) trimmed interest rate by 20bps and its reserve requirement ratio by 50bps to boost loan demand. Another important measure unveiled by the PBoC was a 50bps rate cut for existing mortgages to prop up its property sector.

|

|

|

Fixed Income

In September, the Fed lowered the policy rate by 50bps. Markets had earlier priced in a 25bps rate cut but a slowing job market provided the central bank the stimulus to deliver a larger-than-expected rate cut. Consequently, US Treasury yields declined, with the 10-year yield falling 11bps to 3.81% and the 2-year yield decreasing 25bps to 3.66%. Meanwhile, weak labour market data and falling inflation further widened the spread between 10- and 2-year yields.

In Europe, the ECB cut rates by 25bps amid weakening economic growth and slowing inflation in the region. However they remained cautious, stating that it did not intend to pre-commit to a particular ‘rate path’. The 10-year German Bund yield fell to c.2.1068% in September, while the 10-year UK gilt yield fell to 3.9861% in the month, as the BoE left rates unchanged, stating that a rate cut might become a possibility in the near term if the economy continued to grow in line with expectations.

|

|

|

|

|

Commodities

In September, global commodity markets saw negative returns, as cocoa and oil prices dampened overall gains. Oil prices declined as Saudi Arabia considered moving away from its USD100 per barrel target and signalled a potential increase in production, in line with OPEC+’s plans to boost supply. However, a new stimulus package from China – the top oil importer – helped mitigate further losses. Natural gas prices surged on increased demand for power generation, notably from artificial intelligence datacenters, and the arrival of cold weather in North America and Europe. Gold prices ramped up to an all-time high in September, aided by robust investment demand, a weakening US dollar, geopolitical tensions, falling US real interest rates and central bank purchases. The Fed’s rate cut and the looming uncertainty surrounding the US elections further enhanced gold’s appeal as a safe haven asset. Silver prices also rallied driven by China’s economic stimulus measures, US interest rate cuts, rising demand in the electronic vehicle and green energy sectors, increased festive and jewellery demand and a decline in global production, due to mine closures in Peru and regulatory hurdles in Mexico. Prices of industrial metals, especially copper, surged, supported by China’s economic stimulus and US interest rate cuts. Wheat futures rose, due to dry planting conditions in key regions and supply risks from geopolitical tensions, along with reduced export forecasts. Cocoa prices dropped on increased global supply and favourable weather in leading growers Ivory Coast and Ghana. Coffee prices continued to rise because of adverse weather in Brazil and limited production in Vietnam.

|

|

|

| |

|

|

|

Central Bank Quotes

“Recent inflation data have come in broadly as expected, and the latest ECB staff projections confirm the previous inflation outlook. Staff see headline inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, as in the June projections. Inflation is expected to rise again in the latter part of this year, partly because previous sharp falls in energy prices will drop out of the annual rates. Inflation should then decline towards our target over the second half of next year.”

Christine Lagarde, President, European Central Bank (12 September 2024)

“Democracies around the world, countries that are like the United States, have independent central banks. And the reason is that people have found over time that insulating the central bank from direct control by political authorities avoids making monetary policy in a way that favors, maybe, people in office as opposed to people who are not in office.”

Jerome Powell, Chairman, Federal Reserve (18 September 2024)

|

|

| |

|

|

|

Market Indices

|

| |

|

|

|

In case you missed it

|

|

What’s Ahead

- October 15 – UK: Unemployment Rate

- October 17 – Eurozone: ECB Interest Rate Decision

- October 18 – India: Forex Reserves

- October 23 – Canada: BOC Interest Rate Decision

- October 24 – Japan: Manufacturing and Services PMI

- October 29 – US: Consumer Confidence

- October 30 – Spain: Inflation Rate YoY

- November 1 – ISM Manufacturing PMI

- November 5 – HSBC Composite PMI Final

- November 7 – BoE Interest Rate Decision

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

ABOUT ACUITY KNOWLEDGE PARTNERS

Acuity Knowledge Partners (Acuity) is a leading provider of bespoke research, data management, analytics, talent, and technology solutions to the financial services industry, including asset managers, corporate and investment banks, private equity and venture capital firms, hedge funds and consulting firms. Its global network of over 6,000 analysts and industry experts, combined with proprietary technology, supports more than 650 financial institutions and consulting companies to operate more efficiently and unlock their human capital and transforming operations. Acuity is headquartered in London and operates from 16 locations worldwide.

Acuity was established as a separate business from Moody’s Corporation in 2019, following its acquisition by Equistone Partners Europe (Equistone). In January 2023, funds advised by global private equity firm Permira acquired a majority stake in the business from Equistone, which remains invested as a minority shareholder.

For more information, please visit https://www.acuitykp.com/about-us/

|

|

|

|

|

|

US: +1 929 618 0217 | UK: +44 20 7550 4499 | India: +91 80 6113 3000

Sri Lanka: +94 11 235 6000 | Beijing: +86 10 8248 6812 | HK: +852 3002 4980 | contact@acuitykp.com |

|

|

|

|

|

|

|

|

©2024 Acuity Knowledge Partners. All rights reserved. |

|

|

|

|

|

|