.jpg) |

| |

|

|

| |

As we step into 2025, investors must reassess whether the factors driving strong performance in 2024 will persist. Last year’s impressive gains, driven by the robust US economy and rapid AI growth, have set a strong foundation for the year ahead. While US equities, especially mega-cap tech, have led the market, the investment landscape is evolving. The AI sector is set to grow further, creating opportunities beyond the current tech giants. With US equity valuations at peak levels and tightening credit spreads, diversification is crucial. Emerging markets like China and India offer potential, and European equities remain promising despite challenges. Investors should stay alert to policy changes and economic shifts, ensuring they are not overly concentrated in any asset class or region. A strategic, diversified approach will be vital for navigating the uncertainties of 2025. Flexibility, caution, and a margin of safety will be key lessons from 2024.

Narendra Babu V S, Senior Director, Financial Marketing Services

|

|

| |

|

|

| |

|

|

|

Global Markets

|

|

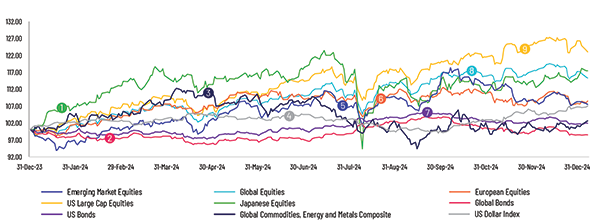

- 1. January 25: Japanese equities surged as foreign investors increased their stakes, drawn by a weakening yen that boosted exporter shares and strong performance in the chip sector – Japanese Equities

- 2. February 23: Global bonds saw yields fall as equity markets hit new highs, driven by Nvidia’s strong results and expectations that the Federal Reserve won’t cut rates until at least June – Global Bonds

- 3. April 15: Copper and aluminum prices surged due to Western bans on Russian metals and increased manufacturing activity in the US and China. – Global Commodities, Energy and Metals Composite

- 4. June 20: The dollar index jumped over 0.25%, fueled by central bank moves and market turbulence, with a rate cut by the Swiss National Bank sending the Swiss franc tumbling and giving the dollar an extra boost. – DXY

- 5. July 13: Taiwan and India now each hold over 19% in the MSCI EM Index, approaching China’s 22.8% share, allowing investors to better diversify by focusing on AI chipmakers and infrastructure development. Emerging Market Equities

- 6. August 19: European stocks surged, led by retail and basic resources, as investors anticipated key data and U.S. Federal Reserve Chair Jerome Powell’s Jackson Hole speech for rate cut signals. – European equities

- 7. September 20: U.S. bond funds saw inflows for the 16th consecutive week, driven by expectations that the Federal Reserve would implement a significant rate cut in its upcoming meeting. – US Bonds

- 8. October 5: Global equities and the dollar surged on strong U.S. labor data, while oil prices saw their biggest weekly gains in a year amid Middle East tensions. – Global Equities

- 9. November 29: US equities hit record highs in a shortened Black Friday session, driven by tech stocks like Nvidia and aided by industrial stocks. – US Equities

|

| |

|

|

|

.jpg)

|

| |

|

|

|

2024 Financial Market Dynamics

|

|

| |

|

|

|

Equities

Global equity markets rallied in 2024, aided by a broad rally in tech stocks, cooling inflation and rate cuts by the central banks. The US equity markets gained on easing inflation and the Federal Reserve’s (Fed’s) rate cuts. A softening job market and easing inflation led the Fed to cut rates by 50 basis points (bps) for the first time in four years in September. The Fed followed it up with two more 25bps cuts. Meanwhile, a hawkish tilt by the Fed at its December meeting, where it stated that future rate cuts would be slower, left investors unhappy. The US presidential election also played a crucial role in the recovery, driven by expectations that President-elect Donald Trump’s policy programme would stimulate growth, reduce taxes and lessen regulation.

European equities advanced, aided by significant outperformance in the information technology sector, backed by a notable drop in annual inflation and interest rates. However, concerns over weak corporate earnings and potential tariffs from the US hampered investor sentiment. The European Central Bank (ECB) cut its key interest rates for the fourth time this year by 25bps in December 2024, boosting monetary policy transmission. The UK market also rose in 2024, led by small- and mid-sized companies and consistent rate cuts by the Bank of England. In Asia, the Japanese equity market rose but remained volatile throughout the second half of the year. The Bank of Japan (BoJ) raised its interest rates to 0.25%, from -0.1% at the beginning of 2024, the highest since 2008, amid uncertainties regarding wage trends and the policies of US President-elect Donald Trump’s administration. Chinese equities gained modestly after the government implemented stimulus measures, including rate cuts and fiscal support, to reverse the broader economic slowdown. However, the second Trump presidency heightened trade and technology tensions, as he pledged to impose tariffs of 60% or more on Chinese manufactured goods during his campaign.

|

|

|

Fixed Income

Global bond markets posted negative returns in 2024 amid variable economic indicators, geopolitical conflicts and monetary policy easing decisions taken by central banks. Inflation levels in major economies remained sticky for most of the year, although they began to ease from Q3, primarily due to lower energy costs. Global investment-grade and high-yield bonds delivered positive returns for the year amid a declining inflation trend and stronger-than-expected growth in select markets. US Treasury yields were volatile during the year but ended higher, as the market anticipated a deceleration in the Fed’s interest rate cuts, particularly following Donald Trump’s win in November. The yield on the US 10-year Treasury climbed from 3.88% to 4.55%, while the 2-year Treasury yield increased slightly from 4.23% to 4.24%.

The spread between the 10-year and 2-year Treasury yields widened over the year, resulting in a positively sloped yield curve entering September. Resilient economic conditions benefitted higher-beta corporate credit overall, causing spreads to narrow considerably. The eurozone’s government bonds recorded positive returns in 2024, supported by easing inflation and interest rate cuts by the ECB to spur growth. Among the largest economies, inflation declined in Germany and France. USD-denominated emerging market (EM) bonds were among the top performers, driven by coupons and a favourable economic backdrop. On the other hand, local currency EM bonds saw negative returns due to the overall weakness of EM currencies as the USD strengthened.

|

|

|

|

Commodities

In 2024, global commodity markets experienced modest gains, with notable performances from coffee, cocoa and natural gas, while wheat futures declined. Coffee and cocoa reached all-time highs, driven by climate change-induced supply disruptions in key regions like Brazil, Vietnam and West Africa, along with shipping disruptions from conflicts in the Red Sea. Coffee prices hit a 47-year high in December. Meanwhile, wheat futures declined due to record global harvests and favourable weather conditions, although geopolitical tensions and potential export restrictions provided some support.

Oil prices were volatile but ended the year with marginal gains. Weakening global demand, particularly from China, amid economic slowdown and recession fears put pressure on oil prices. Despite OPEC+ extending production cuts, increased output from non-OPEC producers like the US led to an oversupplied market. Natural gas prices surged to their highest level since December 2022 due to colder weather forecasts, supply disruptions from hurricanes in the Gulf of Mexico and strong LNG export flows from the US. The ongoing Russia-Ukraine conflict further drove up prices by creating supply uncertainties in Europe.

Precious metals, gold and silver saw significant gains due to increased central bank purchases from EMs and expectations of US monetary easing. Gold reached record highs, while silver hit a 12-year peak, as escalating conflicts in the Middle East and uncertainty surrounding US elections drove demand for these safe-haven assets. However, rising US yields and a strong USD weighed on prices. Copper prices rose despite a nearly 20% drop from its record-high in May, driven by increased demand from renewable energy projects, data centres and electrification technologies and electric vehicles and disruptions at major mines, despite the economic slowdown in major markets like China and rising production costs.

|

| |

|

|

|

Foreign Exchange

The USD had a relatively strong start to 2024 compared with the EUR, JPY and GBP due to uncertainty around interest rate cuts by the major central banks. In fact, the strength of the greenback – which is on track for its biggest yearly rally since 2015 – remained one of the top market stories this year. Towards the middle of the year, however, rising anticipation of rate cut by the Fed weighed on the USD. In September, the USD slid to its lowest level in over a year as markets reacted to a significant 50bps interest rate cut and the Fed’s shift to an easing monetary policy stance. Despite this, by the end of the year, the USD gained significantly, while the EUR fell sharply, primarily by expectations surrounding Trump’s economic policies.

Experts believe that while Trump favours a weak USD in a bid to boost exports, his protectionist policies would have the opposite impact on the USD, boosting it even higher in the near term. A 25-bps rate cut by the Fed in mid-December slightly put pressure on the USD. Additionally, Asian currencies weakened after the Fed signalled a slower pace of rate cuts for the coming year. As global investors responded to the Fed’s consistent hawkish stance and the December rate cut, EM currencies came under pressure, with currencies in Indonesia, Korea, India and other countries falling against the greenback. The Chinese yuan also came under renewed pressure against the USD in anticipation of higher trade tariffs from the US.

|

| |

|

|

|

2025 Economic Outlook

The Organisation for Economic Co-operation and Development (OECD) believes the global economy will remain resilient despite the macroeconomic challenges in 2025. The organisation raised its growth outlook for the global economy, expecting it to grow 3.3% y/y both in 2025 and 2026. GDP growth is projected to moderate in OECD economies compared with the pre-pandemic period, coming in at 1.9% in both 2025 and 2026. Economic growth in non-OECD economies is expected to remain stable, with emerging Asian economies continuing to be the biggest contributors to the global economic growth. US GDP is poised to grow 2.4% in 2025, before slowing to a 2.1% growth in 2026.

The Fed expects to cut rates at a slower pace in 2025 as officials wait to see what policies President-elect Donald Trump will implement and their resulting impact on the economy. Two of the key uncertainties for the US economy would remain rising unemployment and sticky core inflation. The Fed, experts believe, would need to strike the right balance by boosting economic growth while ensuring that the inflation remains close to its target level. The euro area is expected to grow at 1.3% and 1.5% in 2025 and 2026, respectively, as real income growth outpaces inflation. In Japan, the BoJ is expected to hike rates two or three times in 2025, taking the benchmark rate to 1% for the first time in three decades.

The Chinese economy might benefit from the government stimulus measures to boost domestic consumer demand. However, falling consumer confidence amid fears of a potential escalation in the US-China trade war is likely to limit the impact of the policy measures. Finally, the Indian economy is poised to remain the fastest-growing economy in 2025 due to growth in the service sector and strong domestic demand. Overall, 2025 would mark another year of solid economic growth. However, geopolitical tensions remain as key headwinds to the global growth story with the potential to disrupt global supply chains, potentially driving inflation higher and impeding economic growth.

|

| |

|

|

|

Central Bank Quotes

“We’re committed to maintaining our economy’s strength by supporting maximum employment and returning inflation to our 2 percent goal. To that end, today, the Federal Open Market Committee (FOMC) decided to take another step in reducing the degree of policy restraint by lowering our policy interest rate by ¼ percentage point. In our Summary of Economic Projections, Committee participants generally expect GDP growth to remain solid, with a median projection of about 2 percent over the next few years. The median participant projects that the appropriate level of the federal funds rate will be 3.9 percent at the end of next year and 3.4 percent at the end of 2026.”

Jerome Powell, Chairman, Federal Reserve (18 December 2024)

” The Governing Council today decided to lower the three key ECB interest rates by 25 basis points. In particular, the decision to lower the deposit facility rate – the rate through which we steer the monetary policy stance – is based on our updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission. The economy grew by 0.4 per cent in the third quarter, exceeding expectations. The labour market remains resilient. Employment grew by 0.2 per cent in the third quarter, again by more than expected. We stand ready to adjust all of our instruments within our mandate to ensure that inflation stabilizes sustainably at our medium-term target and to preserve the smooth functioning of monetary policy transmission”

Christine Lagarde, President of the European Central Bank (12 December 2024)

|

|

Market Indices

.jpg)

|

| |

|

|

|

In case you missed it

|

| |

|

What’s Ahead

- Jan 15 – UK: Inflation YoY

- Jan 17 – China: GDP YoY

- Jan 20 – Japan: Industrial Production YoY

- Jan 21 – Europe: ECOFIN Meeting

- Jan 24 – India: Manufacturing PMI

- Jan 28 – US: FOMC Meeting

- Feb 3 – Australia: Retail Sales MoM

- Feb 5 – South Korea: Foreign Exchange Reserves

- Feb 6 – UK: BoE Interest Rate Decision

- Feb 7 – Canada: Unemployment rate

|

|

|

| |

|

|

| |

|

|

|